Struggling to bring back Malaysian experts from abroad due to high-income tax concerns?

The Returning Expert Programme (REP) is your ultimate recruitment tool! With a 15% flat tax rate, you can significantly boost your employees’ net take-home pay, making your job offer irresistible!

Core Tax Incentives

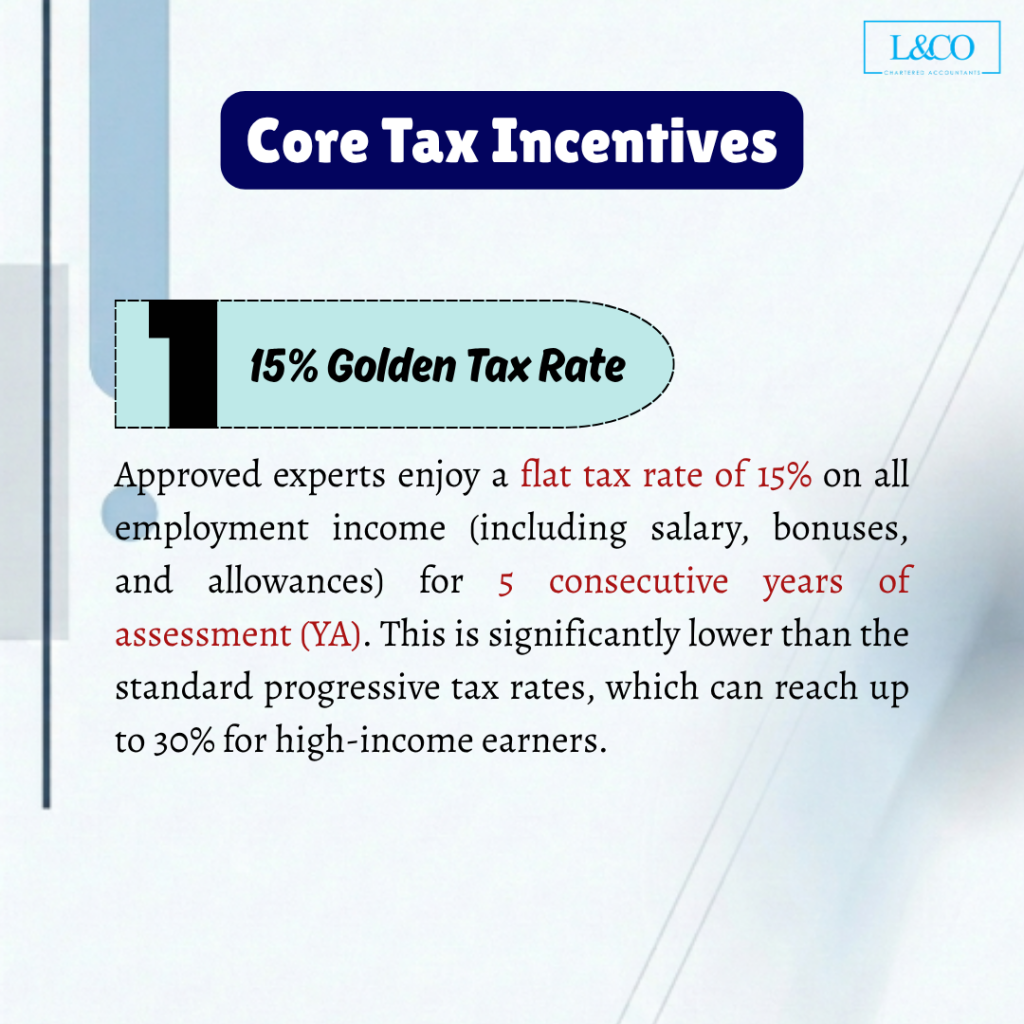

- 15% Golden Tax Rate: Approved experts enjoy a flat tax rate of 15% on all employment income (including salary, bonuses, and allowances) for 5 consecutive years of assessment (YA). This is significantly lower than the standard progressive tax rates, which can reach up to 30% for high-income earners.

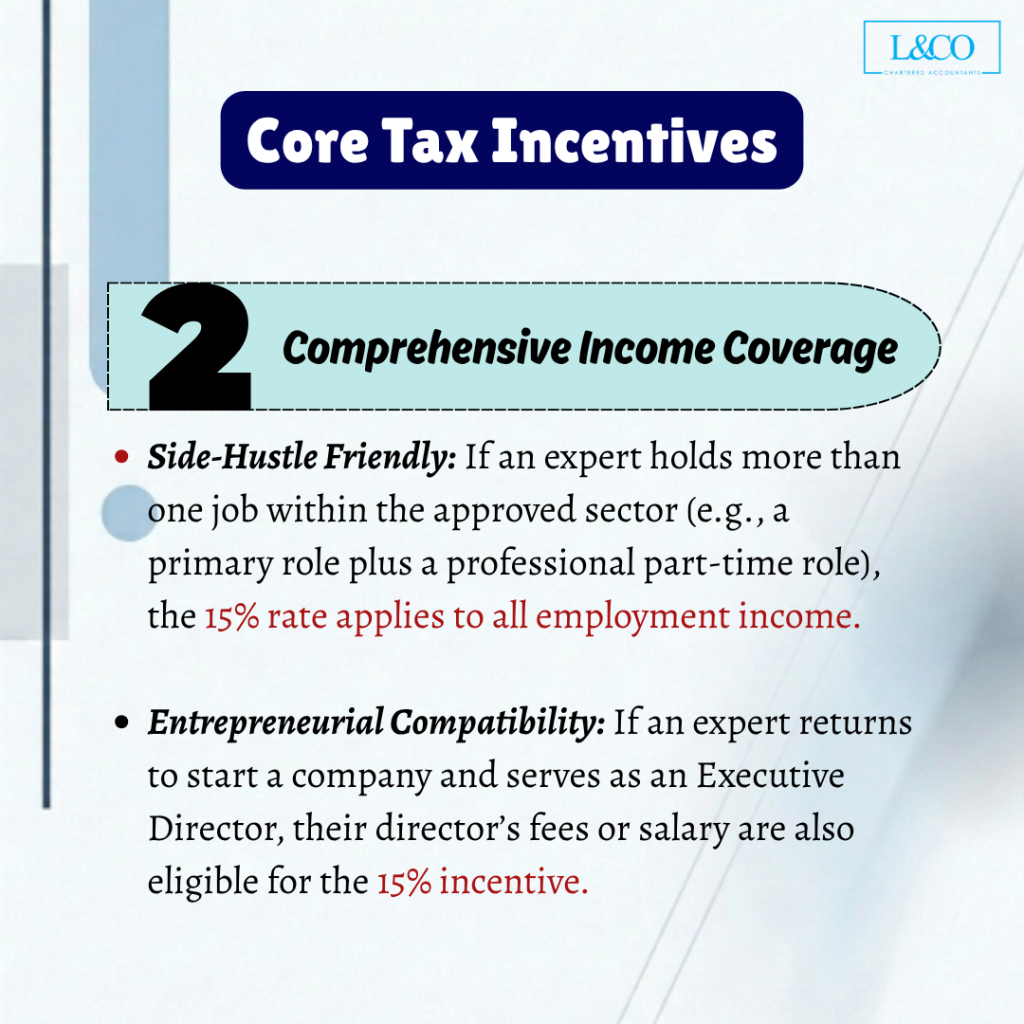

- Comprehensive Income Coverage:

- Side-Hustle Friendly: If an expert holds more than one job within the approved sector (e.g., a primary role plus a professional part-time role), the 15% rate applies to all employment income.

- Entrepreneurial Compatibility: If an expert returns to start a company and serves as an Executive Director, their director’s fees or salary are also eligible for the 15% incentive.

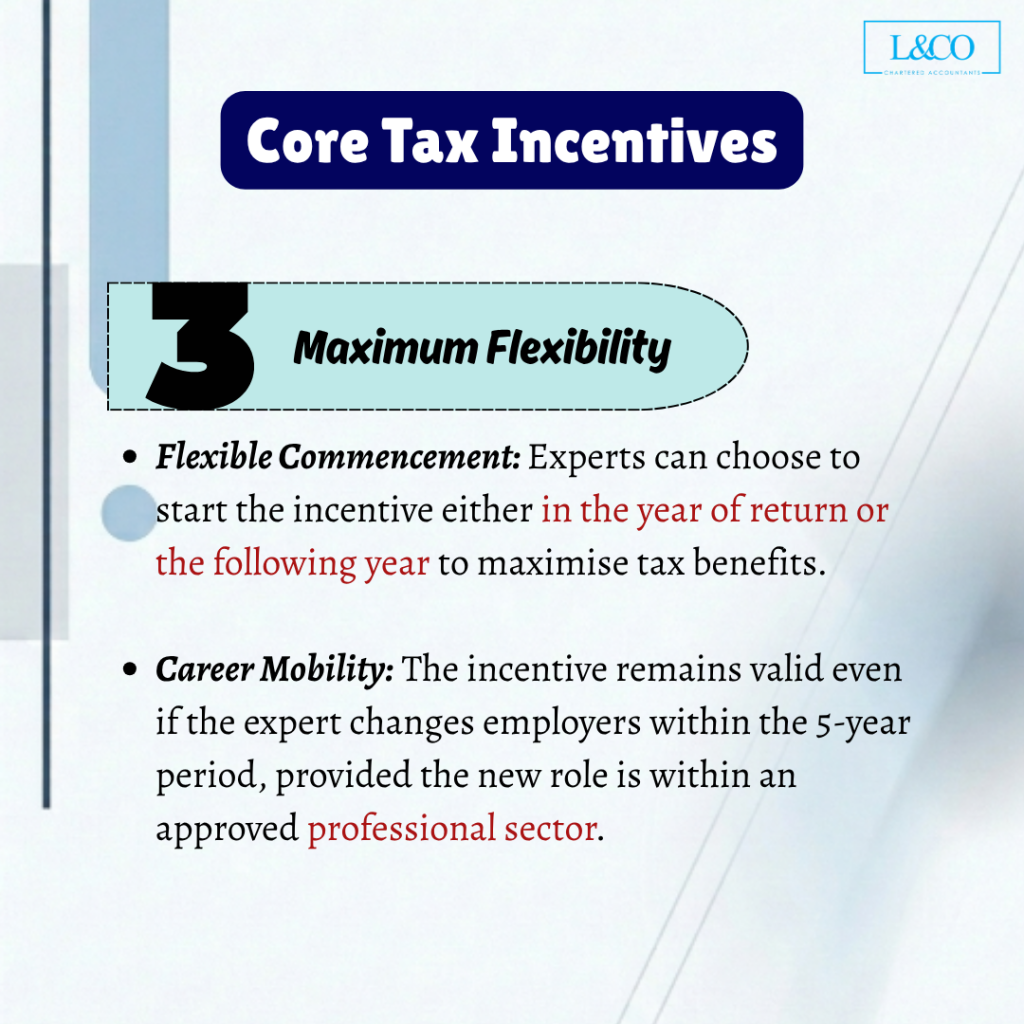

- Maximum Flexibility:

- Flexible Commencement: Experts can choose to start the incentive either in the year of return or the following year to maximize tax benefits.

- Career Mobility: The incentive remains valid even if the expert changes employers within the 5-year period, provided the new role is within an approved professional sector.

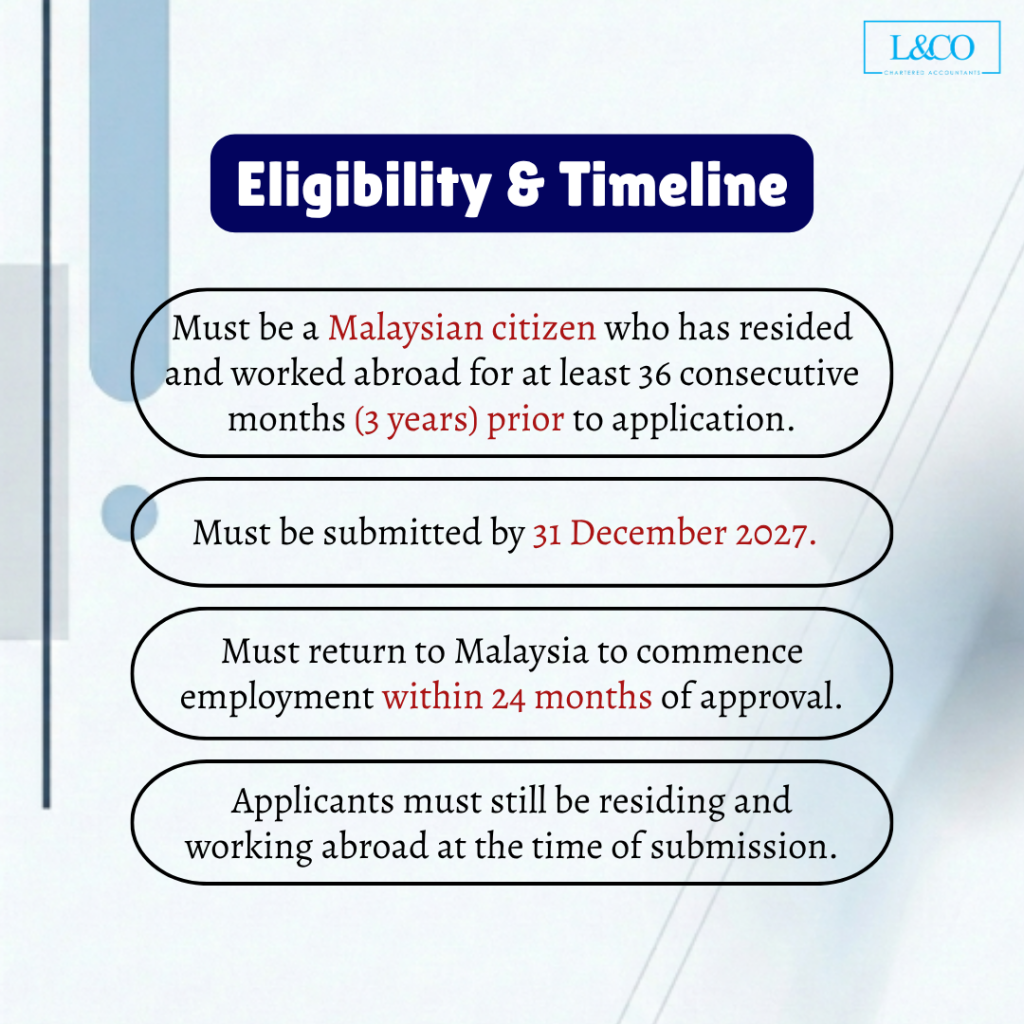

Eligibility & Timeline

- Qualification: Must be a Malaysian citizen who has resided and worked abroad for at least 36 consecutive months (3 years) prior to application.

- Key Deadlines:

- Application Deadline: Must be submitted by 31 December 2027.

- Return Window: Must return to Malaysia to commence employment within 24 months of approval.

- Application Status: Applicants must still be residing and working abroad at the time of submission.

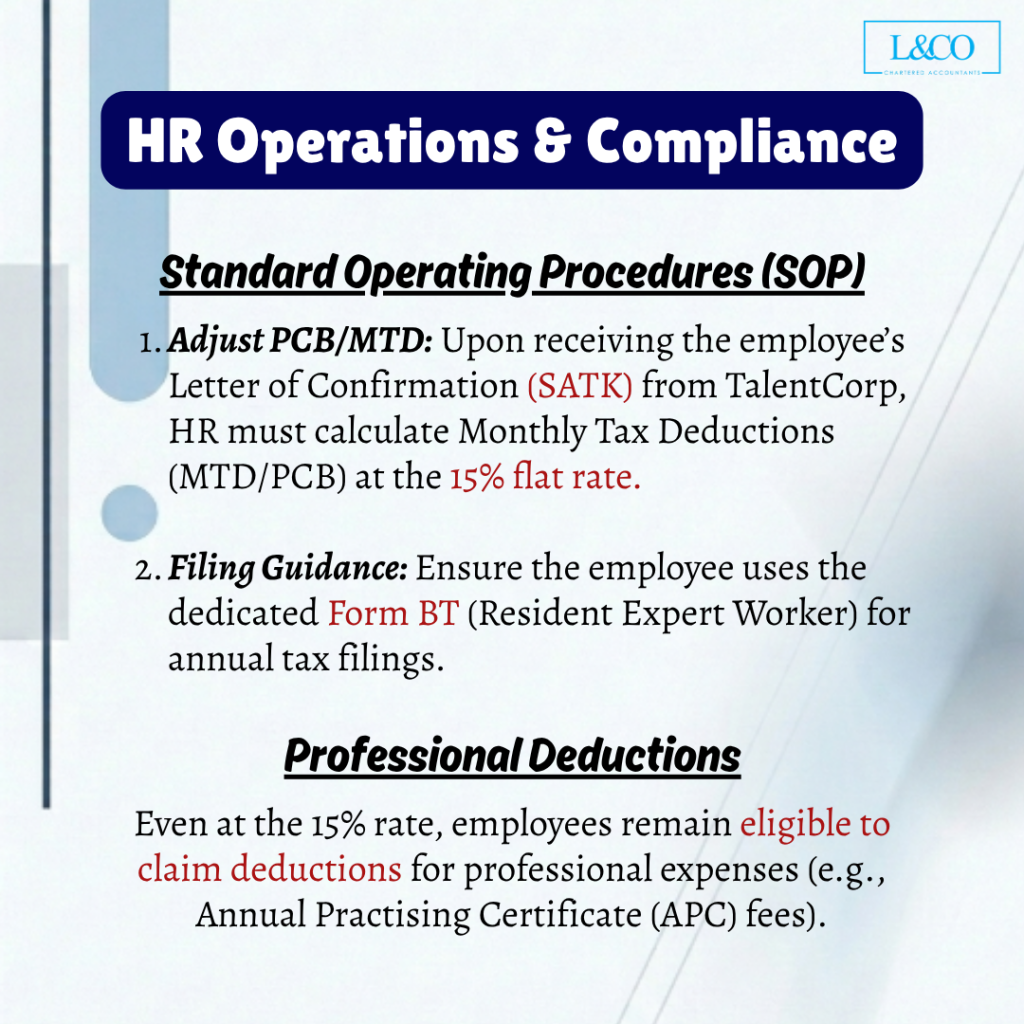

HR Operations & Compliance

Standard Operating Procedures (SOP):

- Adjust PCB/MTD: Upon receiving the employee’s Letter of Confirmation (SATK) from TalentCorp, HR must calculate Monthly Tax Deductions (MTD/PCB) at the 15% flat rate.

- Filing Guidance: Ensure the employee uses the dedicated Form BT (Resident Expert Worker) for annual tax filings instead of the standard Form BE/B.

Professional Deductions:

Even under the 15% rate, employees remain eligible to claim deductions for profession-related expenses (e.g., Annual Practicing Certificate (APC) fees).

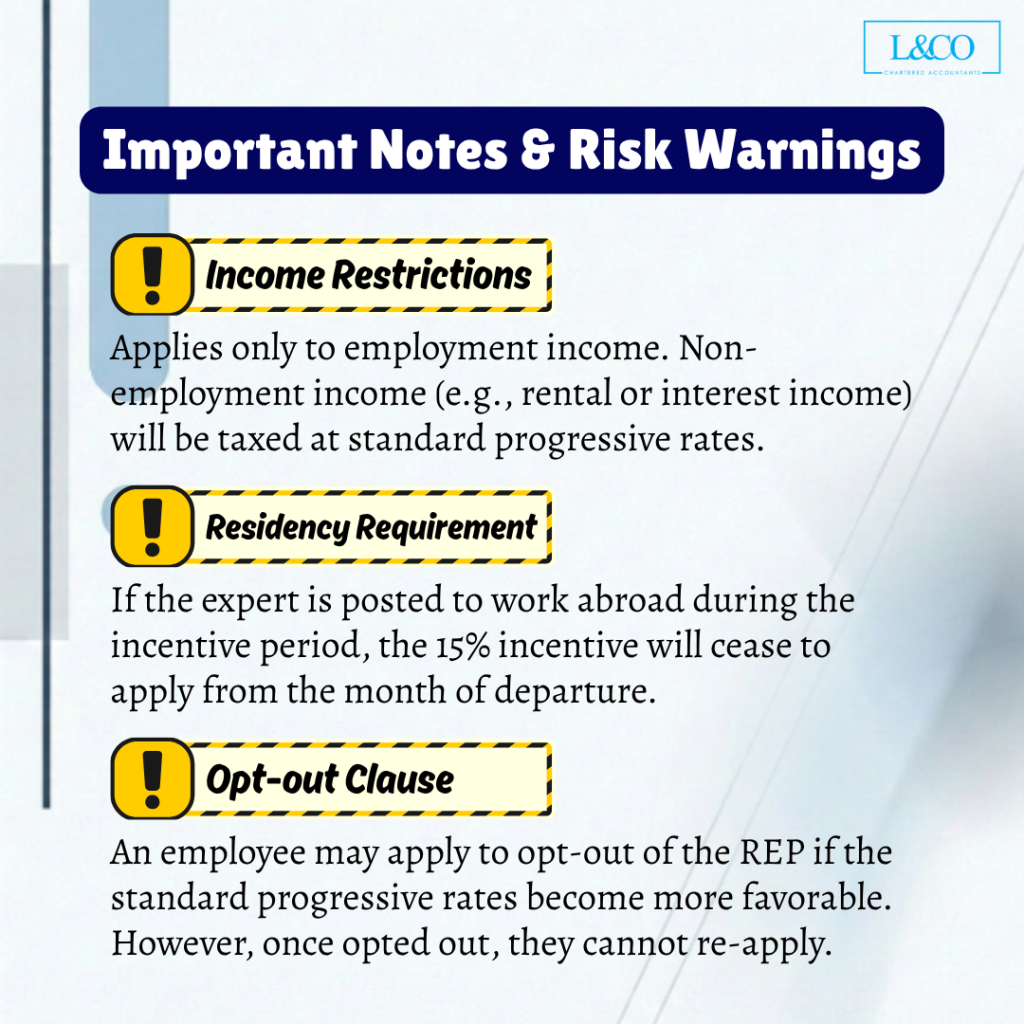

Important Notes & Risk Warnings

- Income Restrictions: Applies only to employment income. Non-employment income (e.g., rental or interest income) will be taxed at standard progressive rates.

- Residency Requirement: If the expert is posted to work abroad during the incentive period, the 15% incentive will cease to apply from the month of departure.

- Opt-out Clause: An employee may apply to opt-out of the REP if the standard progressive rates become more favorable. However, once opted out, they cannot re-apply.

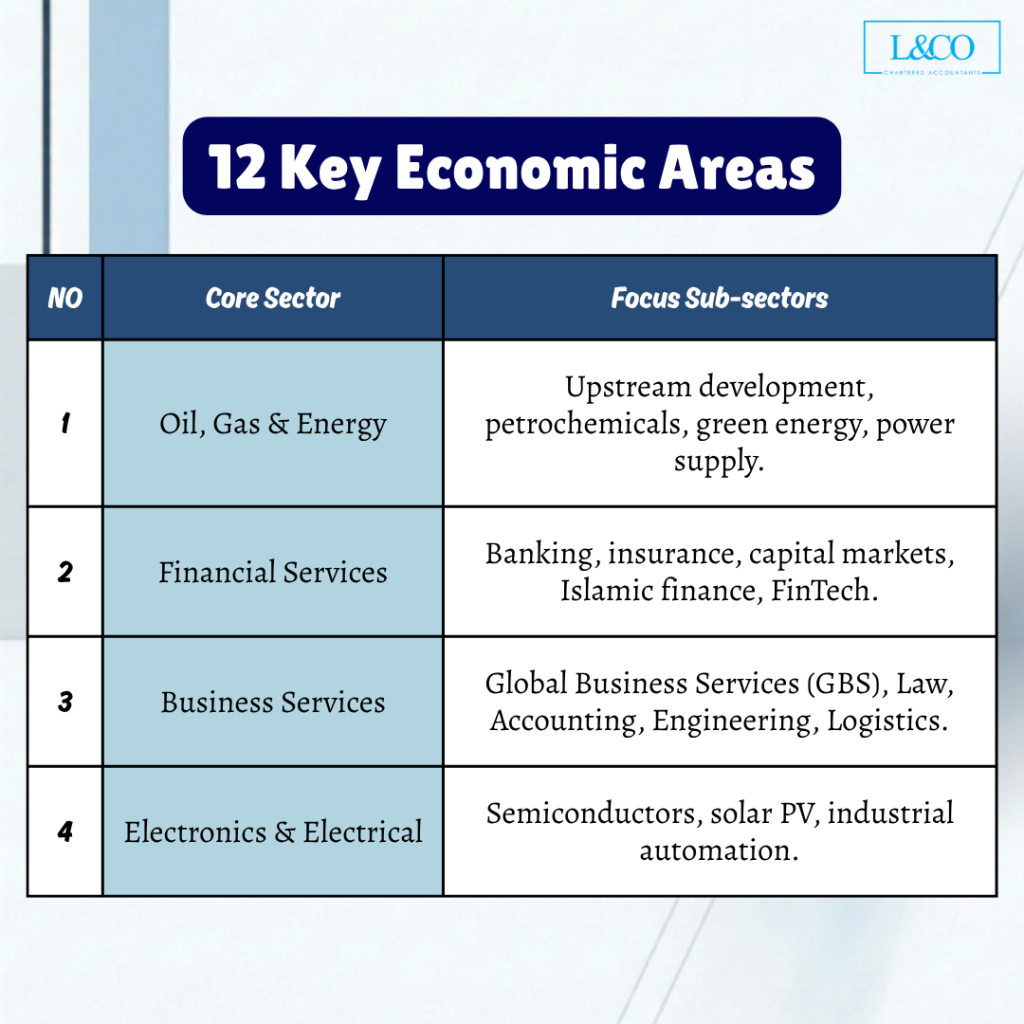

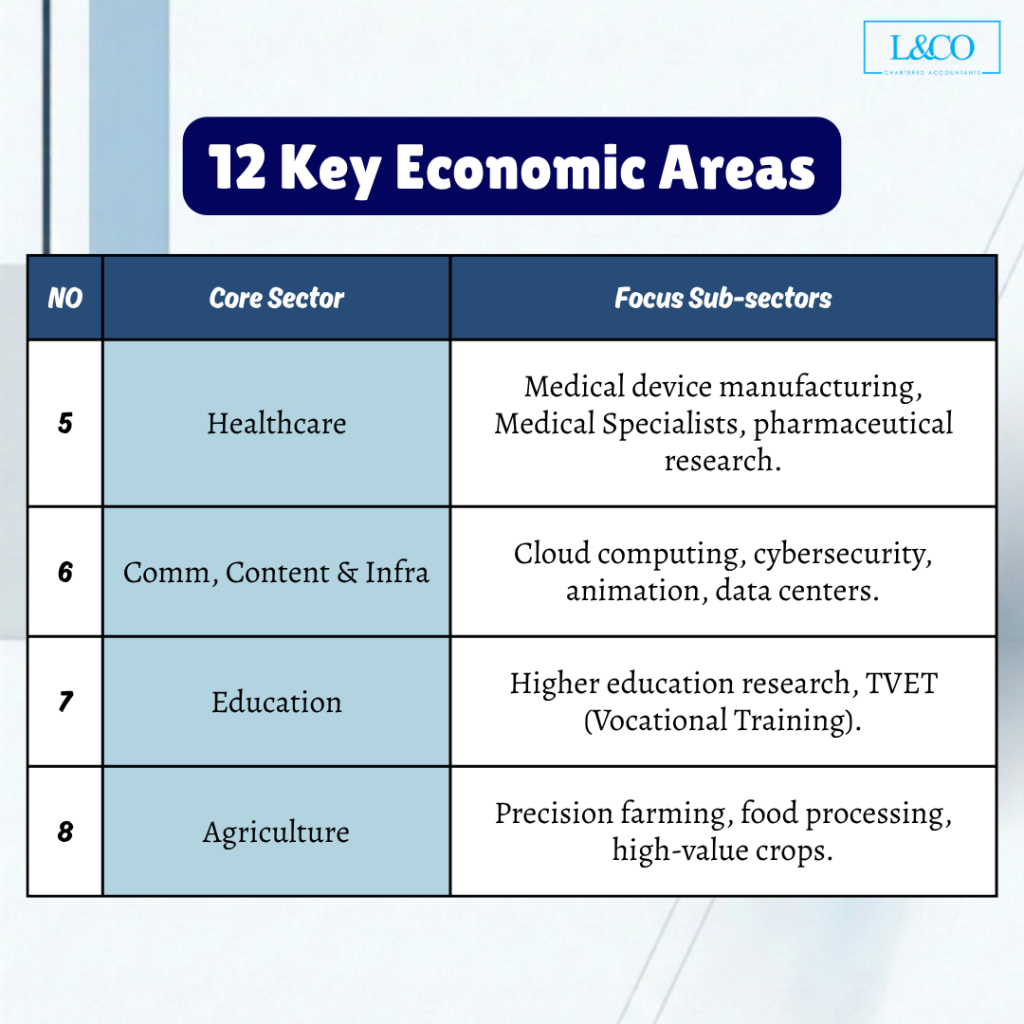

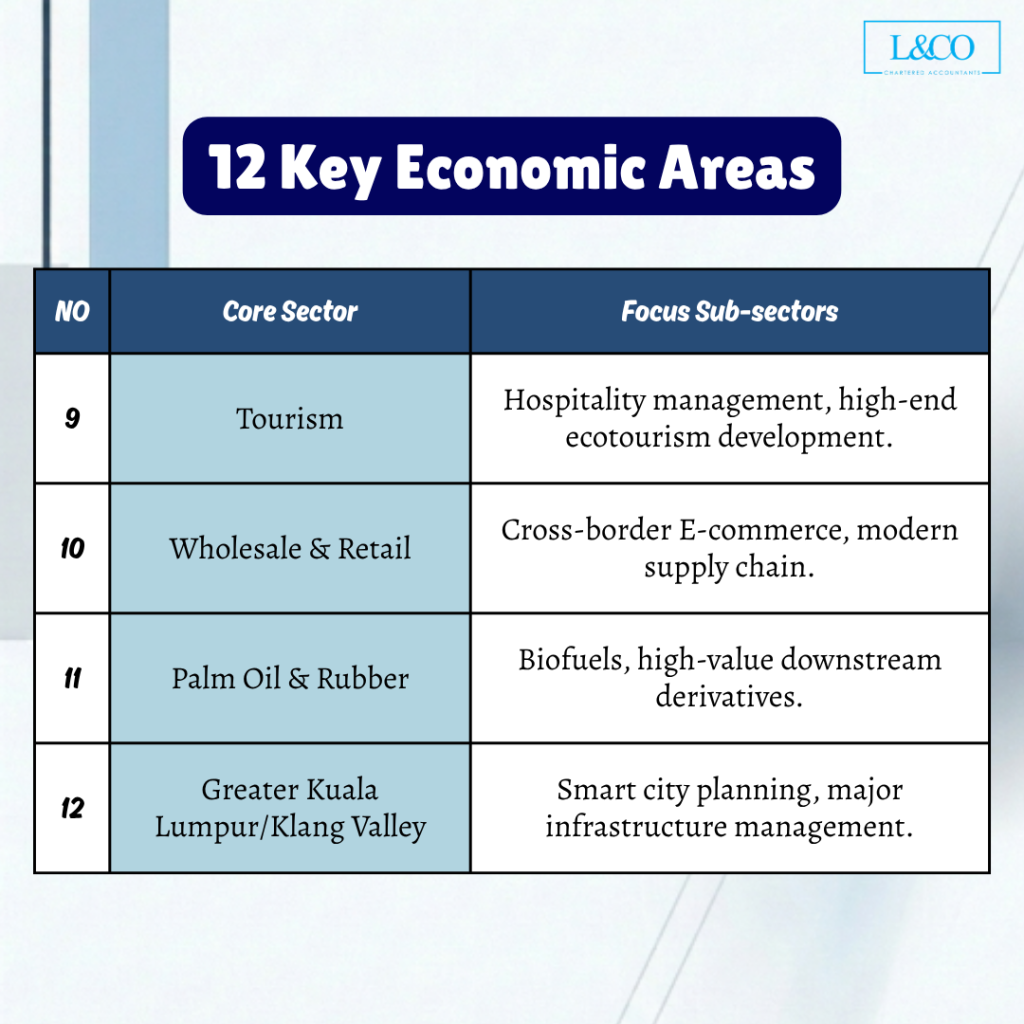

Target Sectors (12 National Key Economic Areas)

| No. | Core Sector | Focus Sub-sectors |

| 1 | Oil, Gas & Energy | Upstream development, petrochemicals, green energy, power supply. |

| 2 | Financial Services | Banking, insurance, capital markets, Islamic finance, FinTech. |

| 3 | Business Services | Global Business Services (GBS), Law, Accounting, Engineering, Logistics. |

| 4 | Electronics & Electrical | Semiconductors, solar PV, industrial automation. |

| 5 | Healthcare | Medical device manufacturing, Medical Specialists, pharmaceutical research. |

| 6 | Comm, Content & Infra | Cloud computing, cybersecurity, animation, data centers. |

| 7 | Education | Higher education research, TVET (Vocational Training). |

| 8 | Agriculture | Precision farming, food processing, high-value crops. |

| 9 | Tourism | Hospitality management, high-end ecotourism development. |

| 10 | Wholesale & Retail | Cross-border E-commerce, modern supply chain. |

| 11 | Palm Oil & Rubber | Biofuels, high-value downstream derivatives. |

| 12 | Greater Kuala Lumpur/Klang Valley | Smart city planning, major infrastructure management. |

**Last Updated on 24.03.2026