Under the dual pressures of inflation and business competition, are your company’s reserve funds still sitting idle in a standard Current Account? Or is your cash flow locked up in Fixed Deposits (FDs)?

.

Introducing the financial instrument increasingly chosen by businesses: the Retail Money Market Fund (RMMF)! An RMMF is a type of unit trust fund that invests in short-term debt instruments with low risk. This fund is established with the aim of providing a stable investment medium and ease in the liquidation of assets.

What is an RMMF?

An RMMF is a type of unit trust fund that invests in short-term debt instruments with low risk. This fund is established with the aim of providing a stable investment medium, ease in liquidation of assets and serves as a temporary investment mechanism for retail investors who are seeking better return than savings accounts without being exposed to high investment risks.

Why Use an RMMF? (Three Core Benefits)

- Superior Daily Returns: Earn higher rates than standard savings or current accounts. Interest is calculated daily, ensuring your idle cash works for you every single day.

- High Liquidity: Unlike Fixed Deposits, there are no penalties for early withdrawal. You can liquidate assets instantly to meet urgent cash flow demands.

- Tax Efficiency & Compliance: Features a transparent, corporate-friendly tax mechanism. It simplifies accounting and ensures your company remains fully compliant with Malaysian tax regulations.

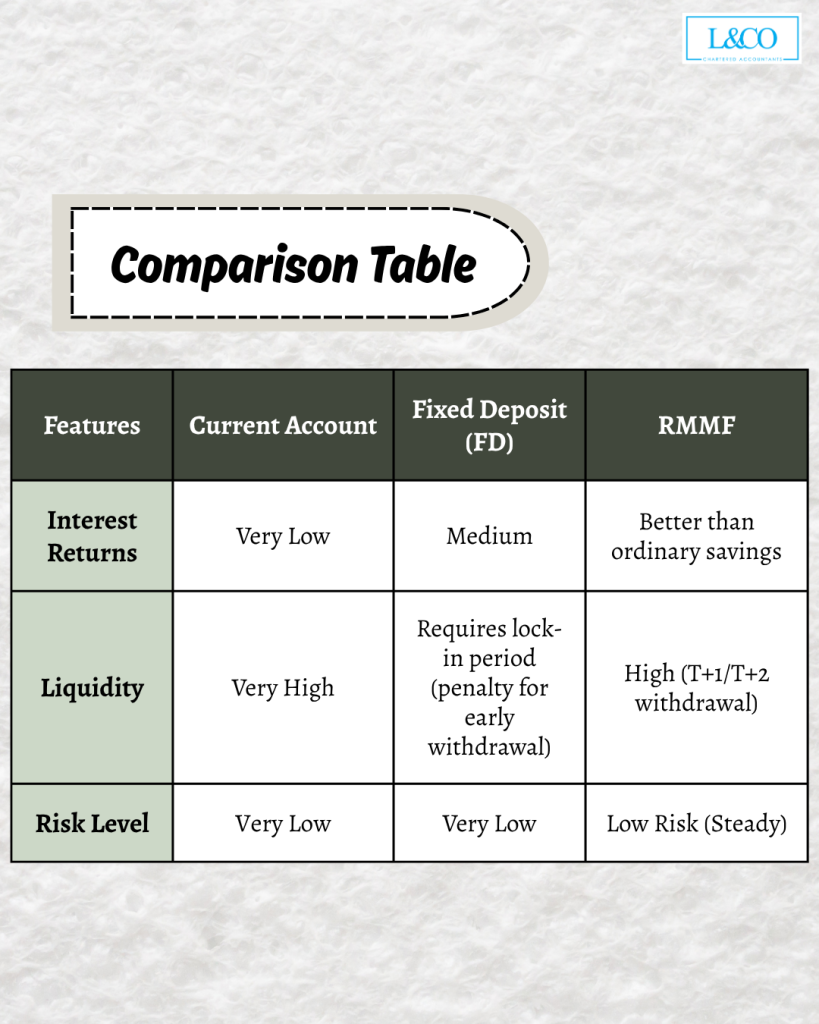

Comparison Table

| Features | Current Account | Fixed Deposit (FD) | RMMF (Retail Money Market Fund) |

| Interest Returns | Very Low | Medium | Better than ordinary savings |

| Liquidity | Very High | Requires lock-in period (penalty for early withdrawal) | High (T+1/T+2 withdrawal) |

| Risk Level | Very Low | Very Low | Low Risk (Steady) |

How is it taxed?

- Taxable for Corporates: RMMF income is tax-exempt for individual investors. However, for resident companies (like your Sdn Bhd), the distributed income is taxable.

- 24% Withholding Tax: The RMMF is required to automatically deduct a 24% withholding tax on the gross interest income distributed to non-individual unit holders.

- Claimable Tax Credits: Corporate unit holders are eligible to claim this 24% deduction as a tax credit under subsection 110(9A) of the ITA. Think of it as an advance tax payment that can directly offset your year-end corporate tax liabilities.

- Clear Documentation: If an RMMF deducts withholding tax, the income is legally considered taxable, even if the voucher labels it as “non-taxable”. The “Taxable Income” column on the voucher clearly indicates the distributed portion, making accounting straightforward.

**Last Updated on 23.03.2026