Many people believe that societies, associations, chambers of commerce, and other non-profit organizations are automatically exempt from income tax. However, under the Malaysian Income Tax Act and Public Ruling No. 1/2015, the tax treatment depends primarily on the source and nature of the income, rather than whether the organization is classified as non-profit.

Therefore, properly distinguishing between member income and non-member income is essential for tax compliance.

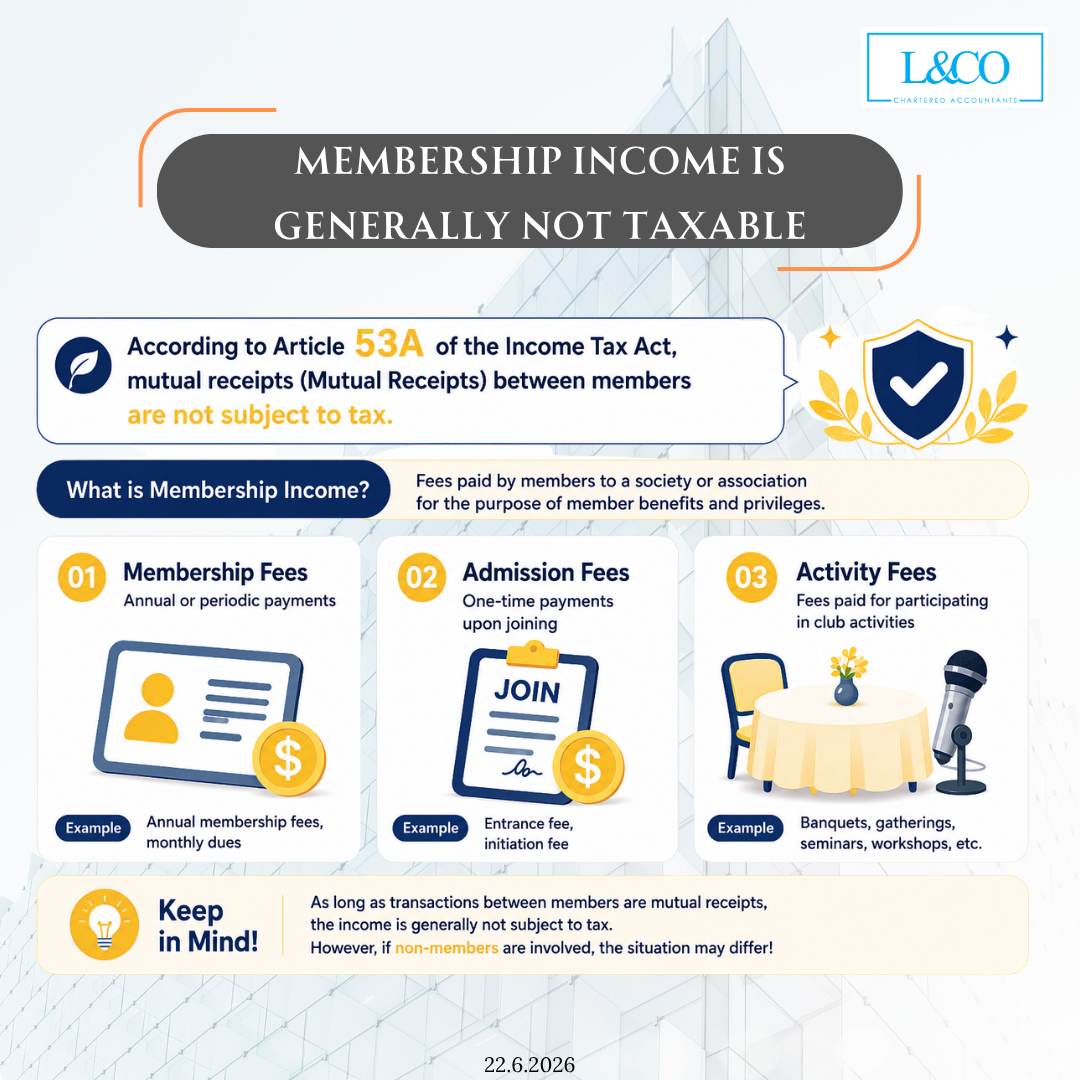

1. Member Income

Under Section 53A of the Income Tax Act, income arising from the principle of mutuality among members is generally not subject to income tax.

Common examples of member income include:

- Annual membership fees

- Entrance or registration feesMember activity fees

Charges for events that are exclusively open to members

These are considered Mutual Receipts and are generally treated as non-taxable income.

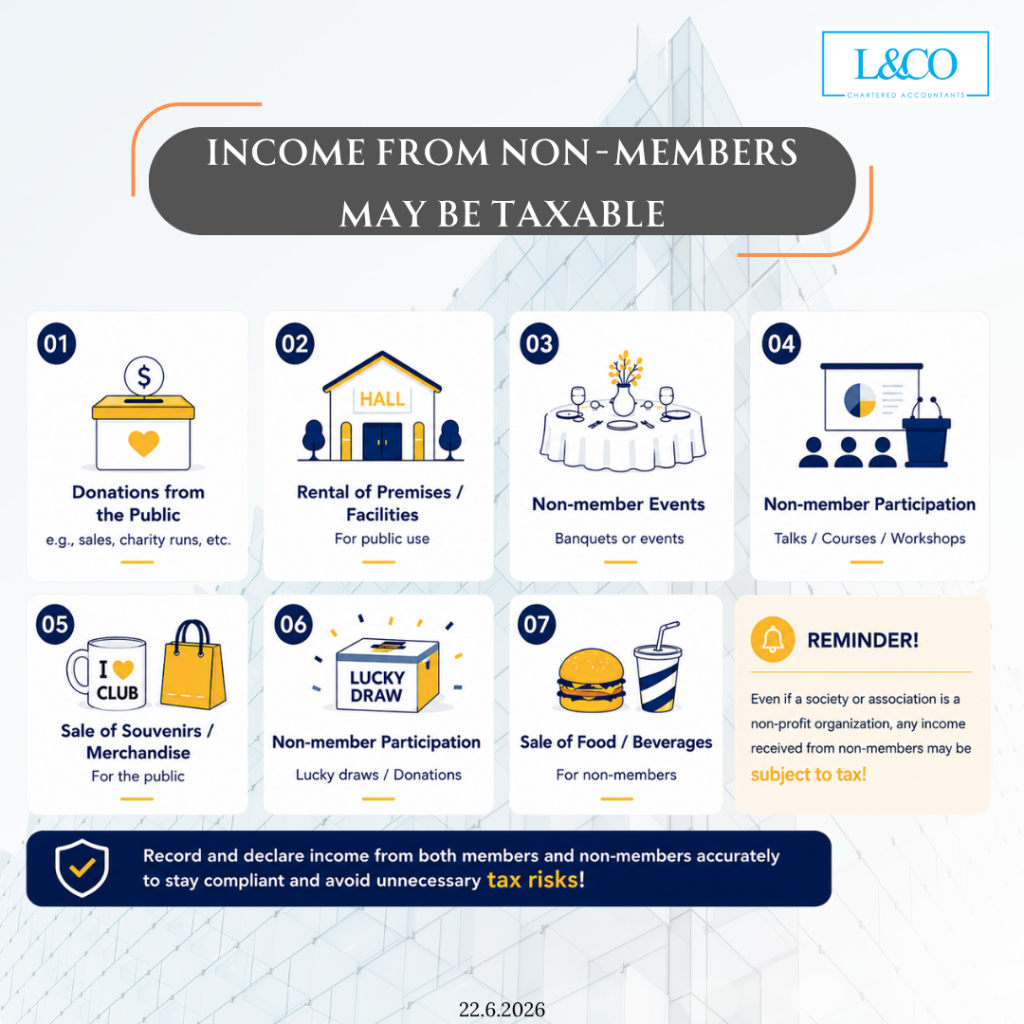

2. What Types of Income May Be Taxable?

When income is derived from non-members or external sources, it may be subject to income tax.

Common examples include:

- Public Fundraising

Income generated through charity sales, fundraising campaigns, or public donation drives. - Rental of Halls, Venues, or Facilities

Even if the organization is non-profit, rental income earned from leasing halls or facilities to the public is generally taxable. - Activities Open to Non-Members

Fees collected from non-members attending dinners, seminars, training courses, workshops, or other events may be taxable. - Sale of Merchandise or Souvenirs

Revenue generated from selling souvenirs, branded merchandise, or other products. - Lucky Draws or Donation Campaigns Involving Non-Members

If these activities are open to the public, the related income should be assessed in accordance with tax regulations.

3. Family Members Are Not Automatically Considered Members

A common misconception is that a member’s spouse, parents, or children are automatically treated as members.

In reality, a member for tax purposes generally refers to an individual who:

- Has voting rights

- Participates in the management of the organization

- Has effective control over the affairs of the organization

Therefore, even if a member’s spouse or child attends an event and pays a fee, the payment may still be regarded as non-member income and may be subject to tax assessment.

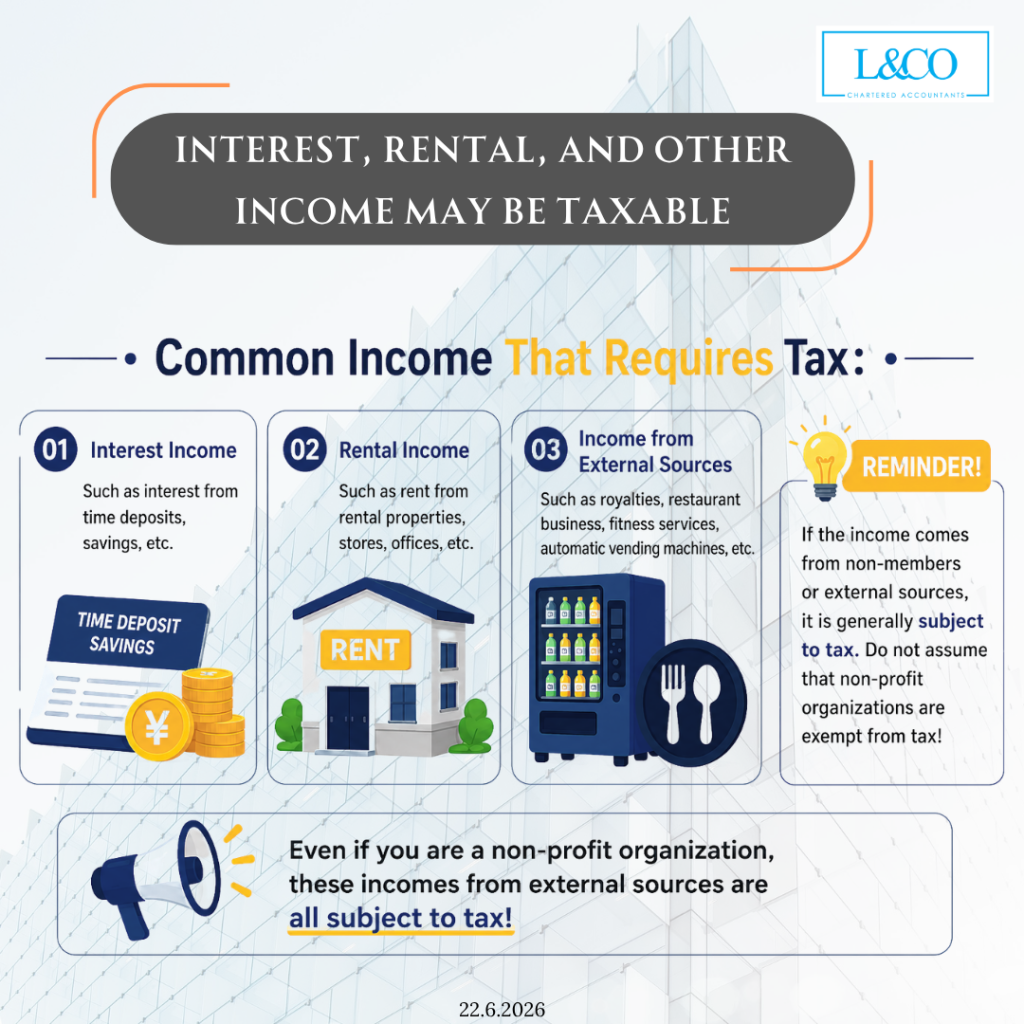

4. Interest, Rental & External Business Income

Apart from member and non-member income, the following are generally regarded as external source income:

- Fixed deposit interest

- Savings account interest

- Rental income from halls, shops, or office premises

- Restaurant operating income

- Gym operating income

- Vending machine income

- Outsourced business operation income

These types of income are generally taxable and do not automatically qualify for tax exemption simply because the organization is non-profit.

5. Outsourcing Business Operations Does Not Automatically Qualify for Tax Exemption

Many societies, associations, and non-profit organizations outsource the operation of facilities such as restaurants, gyms, or vending machines to third parties and receive rental income or operating revenue in return.

However, outsourcing business activities does not automatically make such income tax-exempt. If the income is derived from external sources rather than from mutual dealings among members, the organization may still be subject to income tax, even if it is a non-profit entity.

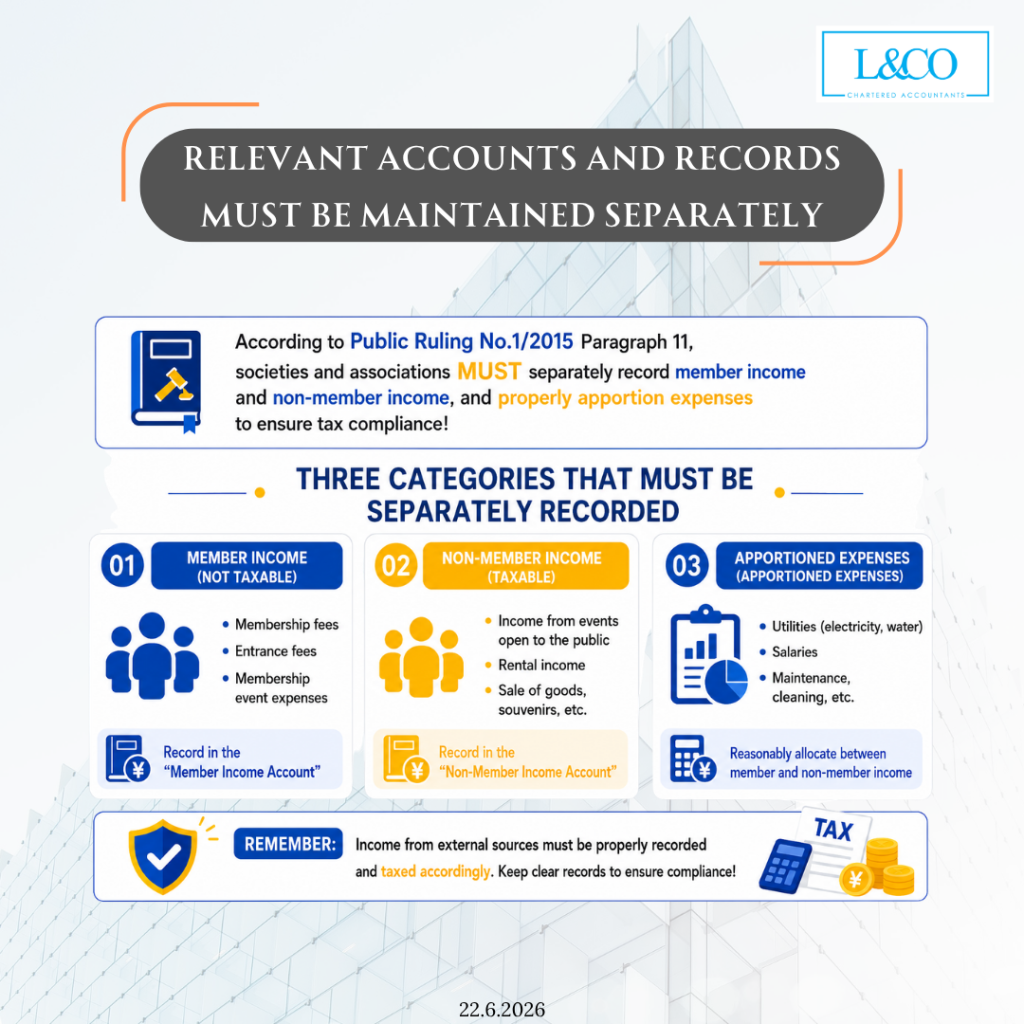

6. Separate Accounting Records Are Essential

According to Public Ruling No. 1/2015, organizations should maintain proper accounting records and clearly separate at least the following three categories:

1. Member Income (Generally Non-Taxable)

- Membership fees

- Entrance fees

- Member activity charges

2. Non-Member Income (Potentially Taxable)

- Public events and activities

- Hall or venue rental

- Merchandise and souvenir sales

- Fundraising income

3. Reasonable Allocation of Expenses

Including:

- Utilities

- Salaries and wages

- Cleaning and maintenance costs

- Administrative expenses

Proper allocation of shared expenses between member-related and non-member-related activities helps ensure tax compliance and minimizes potential disputes during tax audits.

7. Non-Profit Organizations Do Not Automatically Mean No Tax Filing Is Required

According to the principles set out in Public Ruling No. 1/2015, different sources of income are subject to different tax treatments.

1. Membership Income (Generally Non-Taxable)

Membership fees, entrance fees, and charges for members’ activities are considered mutual receipts between members and are generally not regarded as taxable income.

2. Non-Membership Income (May Be Taxable)

Income derived from organizing events for the public, renting out halls, selling merchandise or souvenirs, and fees collected from spouses, parents, children, or other non-formal members may be considered taxable income.

3. Rental and Interest Income (Generally Taxable)

Regardless of whether the income is received from members or non-members, income derived from fixed deposit interest, rental income, vending machine revenue, restaurant operations, or other external sources is generally subject to income tax.