Under the Malaysian tax system, in addition to employees preparing Form EA, companies that provide incentives to Agents, Dealers, or Distributors must also comply with the requirements of Form CP58.

Many businesses overlook the importance of this document, only realizing during a tax audit that it was not prepared on time, which could result in penalties. This article provides a systematic explanation of the applicability, legal basis, threshold amounts, and deadlines for Form CP58.

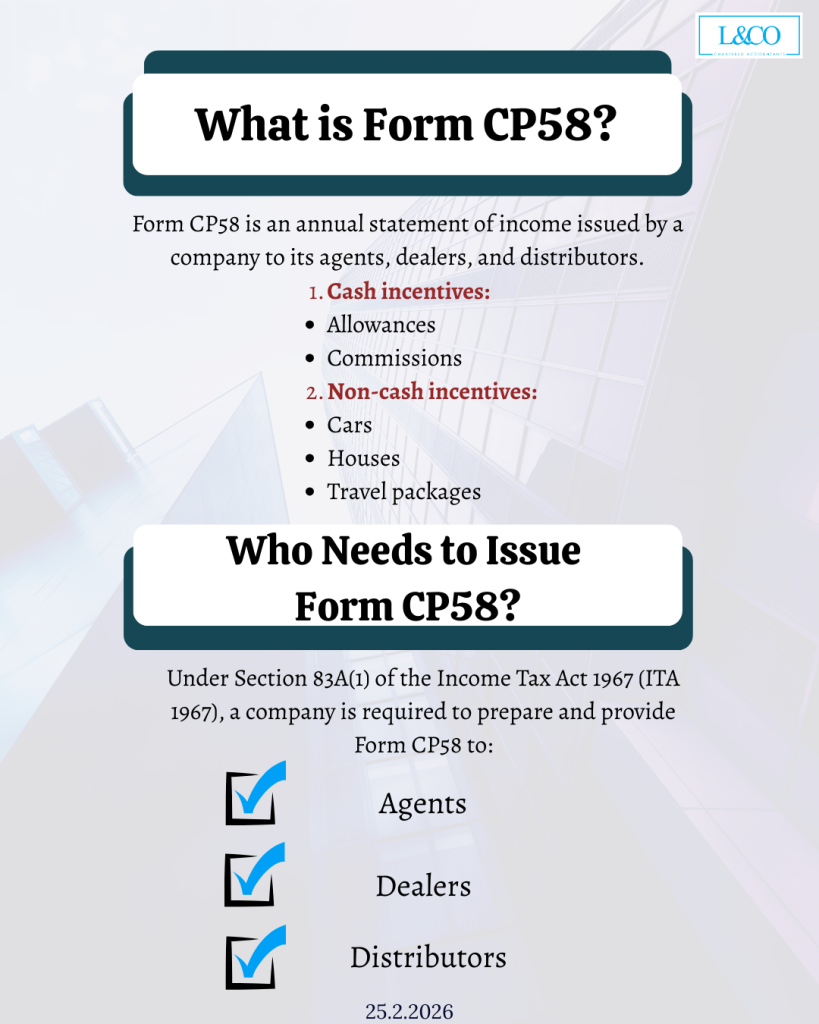

What is Form CP58?

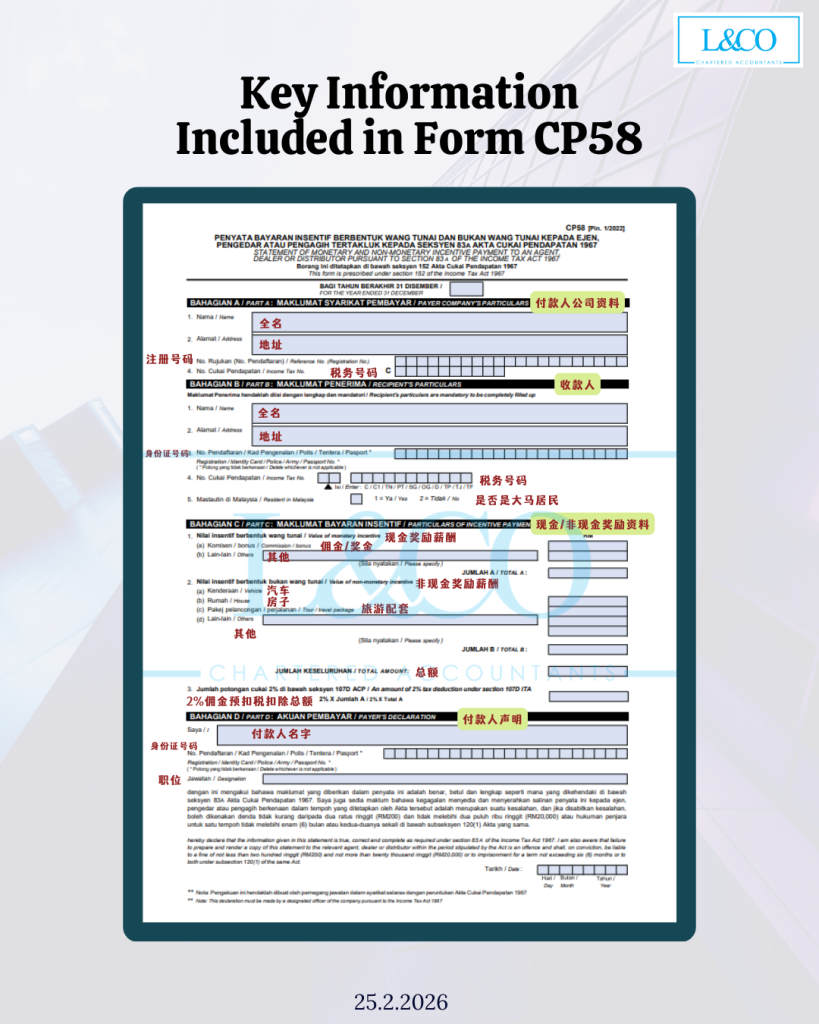

Form CP58 is an annual income statement issued by a company to its agents, dealers, and distributors.

The form details the rewards and incentives paid to relevant parties during the basis year, including:

1.Cash Rewards

- Allowances / Commissions

2. Non-Cash Rewards,

- Cars

- Properties

- Travel packages

- Other benefits-in-kind

The document primarily serves as a reference for agents when reporting their income for tax purposes.

Who Must Receive Form CP58?

Under Section 83A(1) of the Income Tax Act 1967, a company is required to prepare and provide Form CP58, in accordance with the Lembaga Hasil Dalam Negeri (LHDN) requirements, to:

- Agents

- Dealers

- Distributors

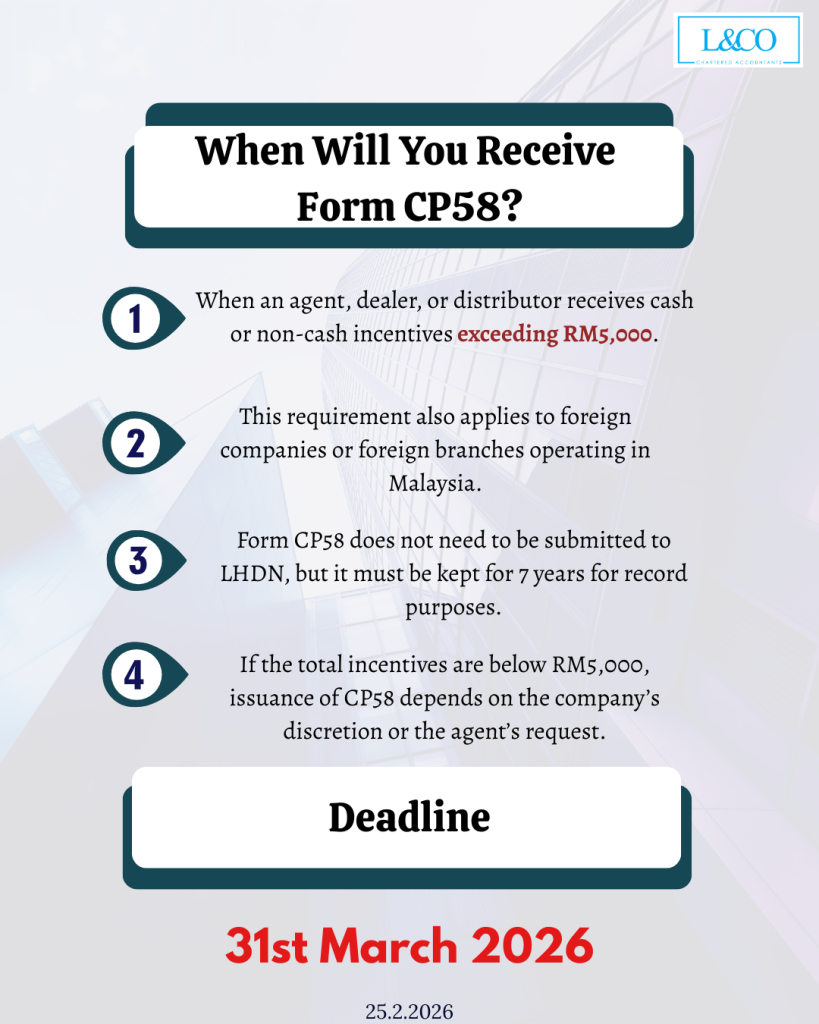

This requirement also applies to foreign companies and their branches operating in Malaysia.

When Must Form CP58 Be Issued?

Total Incentives Exceeding RM5,000

If, in a given year, the total rewards paid to an agent (including cash and non-cash incentives) exceed RM5,000, Form CP58 must be issued.

Rewards can include cash, gifts, vouchers, travel incentives, and other forms of benefits.

Total Incentives Below RM5,000

If the total annual incentives are below RM5,000, the company is not required to issue Form CP58.

However, if the agent submits a written request, the company must provide it.

Deadline

31 March 2026

Companies must issue Form CP58 to qualifying agents, dealers, or distributors on or before the deadline.

Form CP58 Filing Complete Guide

**Data updated on 26.02.2026