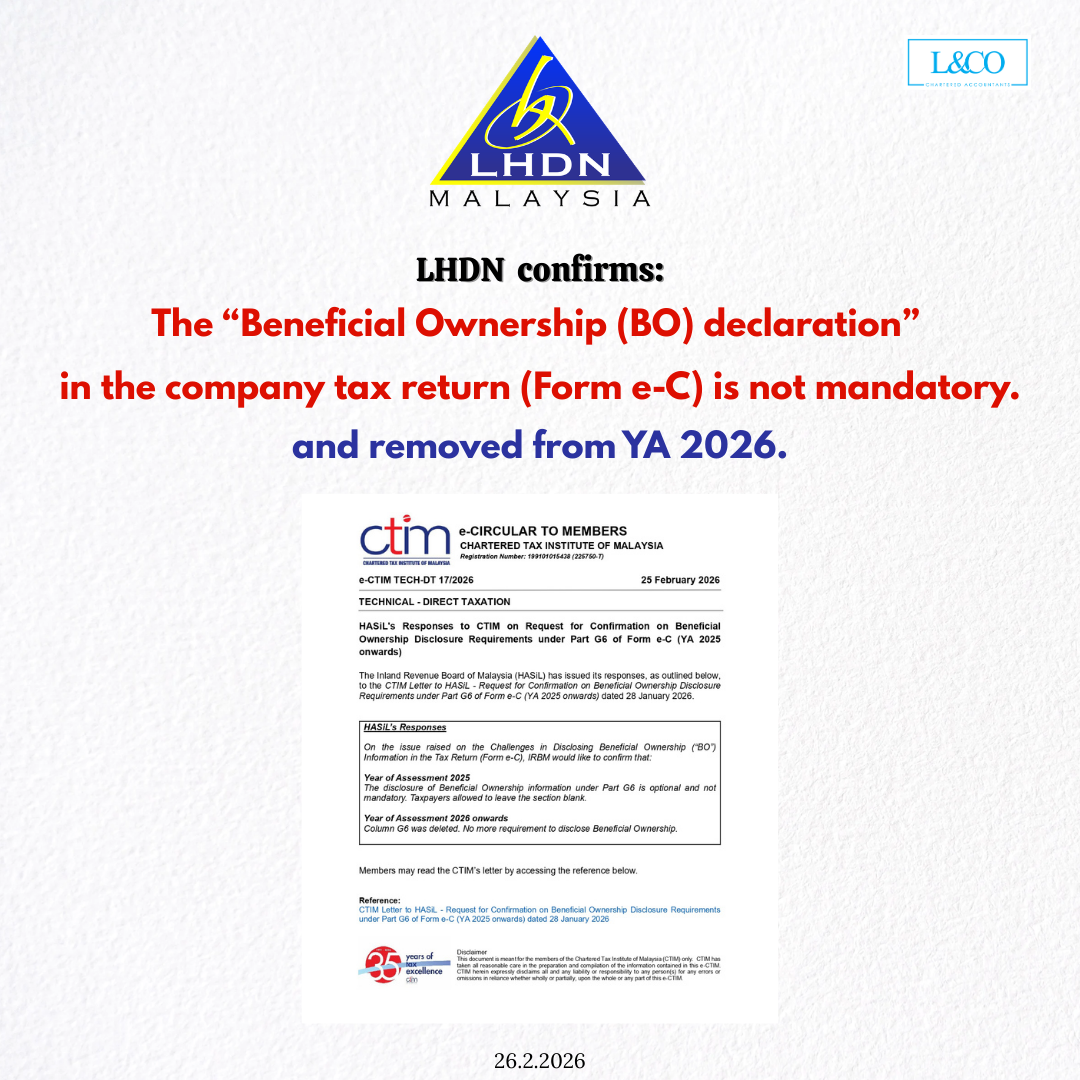

Many companies have raised concerns on whether Beneficial Ownership (BO) information must be disclosed in Form e-C when filing their corporate income tax returns.

This issue has now been officially clarified.

Based on an e-Circular issued by the Chartered Tax Institute of Malaysia (CTIM), which cites the official written response from the LHDN , the following confirmations were provided in relation to Part G6 of Form e-C (Beneficial Ownership disclosure):

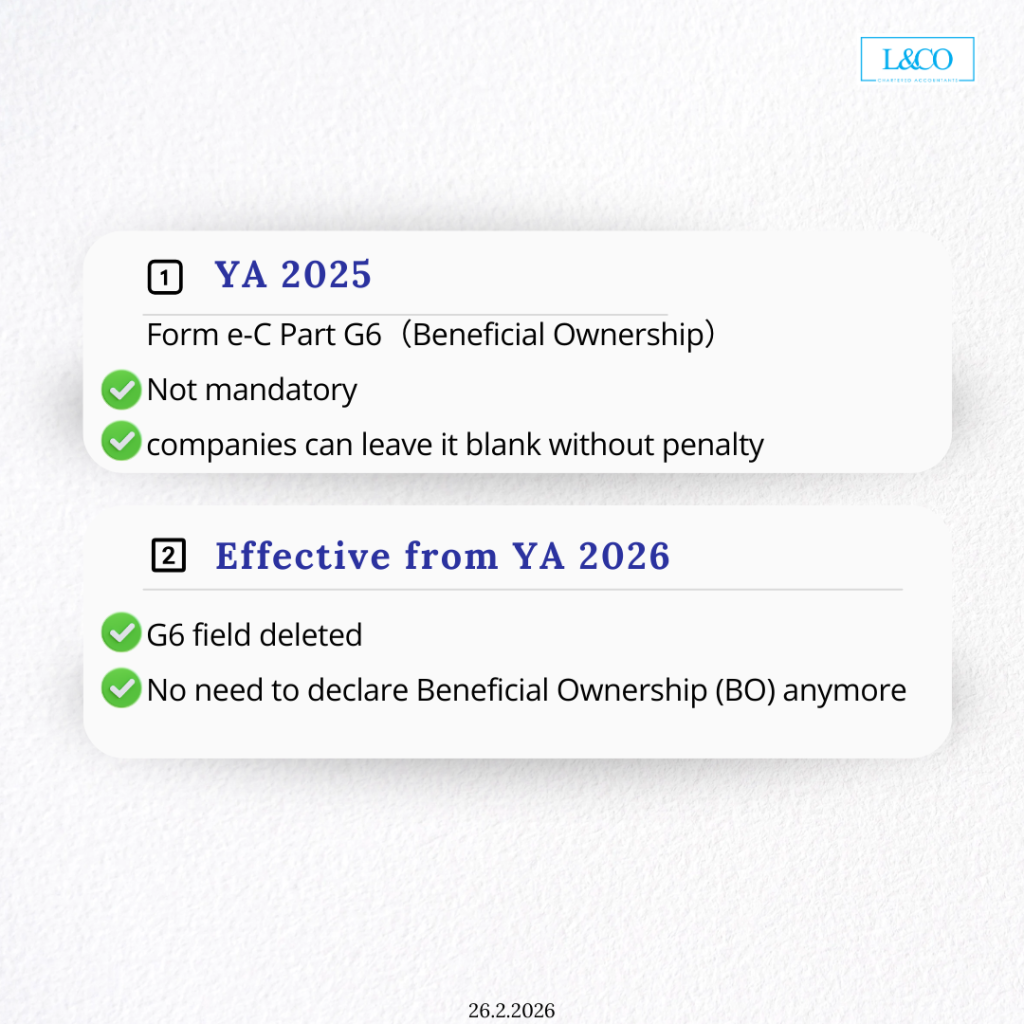

Year of Assessment (YA) 2025

For the Year of Assessment 2025:

- Disclosure of Beneficial Ownership under Part G6 of Form e-C is optional

- Taxpayers are allowed to leave the section blank

- No offence, penalty, or non-compliance issue will arise from non-disclosure

Year of Assessment (YA) 2026 Onwards

From the Year of Assessment 2026 onwards:

- Part G6 has been removed from Form e-C

- There is no longer any requirement to disclose Beneficial Ownership information

Key Takeaway

Companies filing Form e-C for YA 2025 are not required to disclose Beneficial Ownership details, and from YA 2026 onwards, such disclosure is no longer applicable as the relevant section has been removed entirely.

This clarification provides certainty to taxpayers and should help ease compliance concerns when preparing corporate income tax returns.

**Data updated on 27.2.2026