Whether you’re buying or selling property in Malaysia — this is what you need to know. Malaysia RPGT (Real Property Gains Tax) — Latest 2026 Updates ⬇️

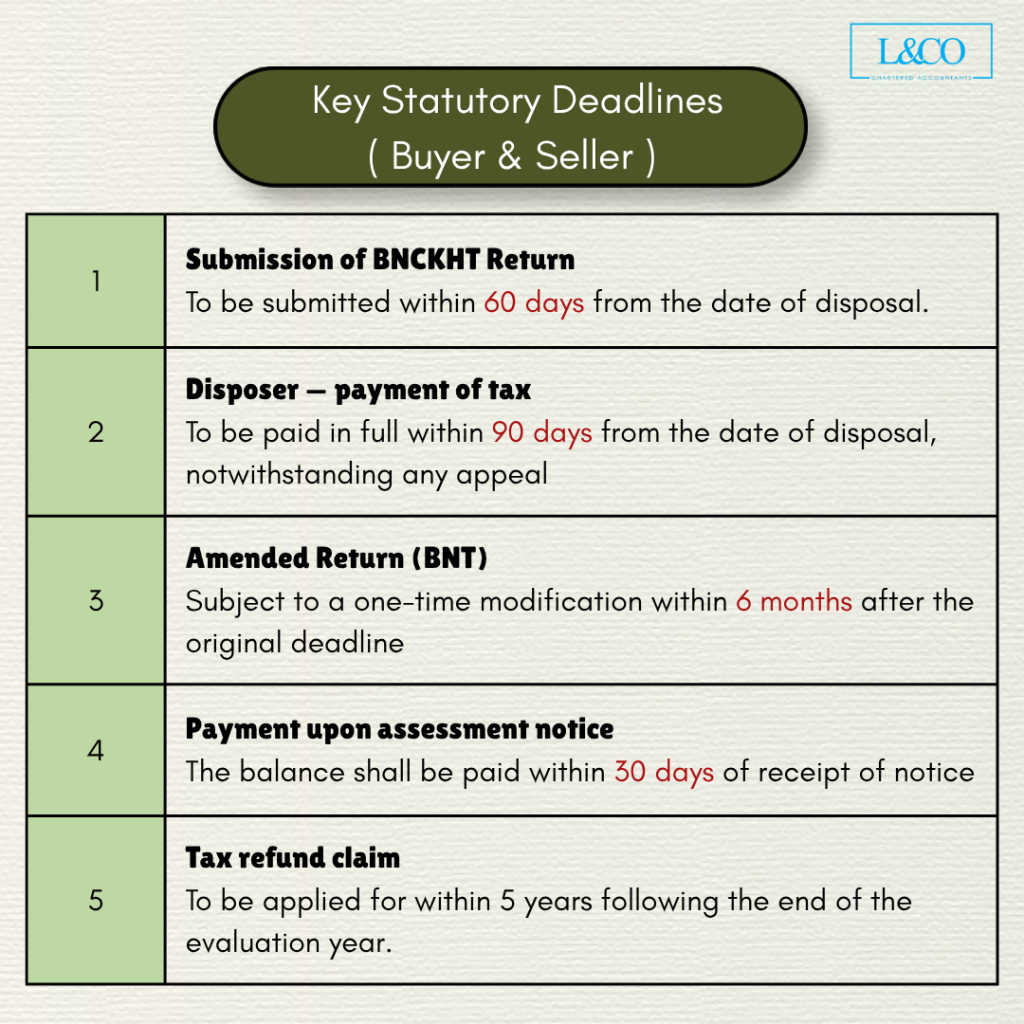

1. Key Statutory Deadlines

Both the acquirer and disposer must strictly observe the following timelines. Non-compliance may result in financial penalties and/or legal action.

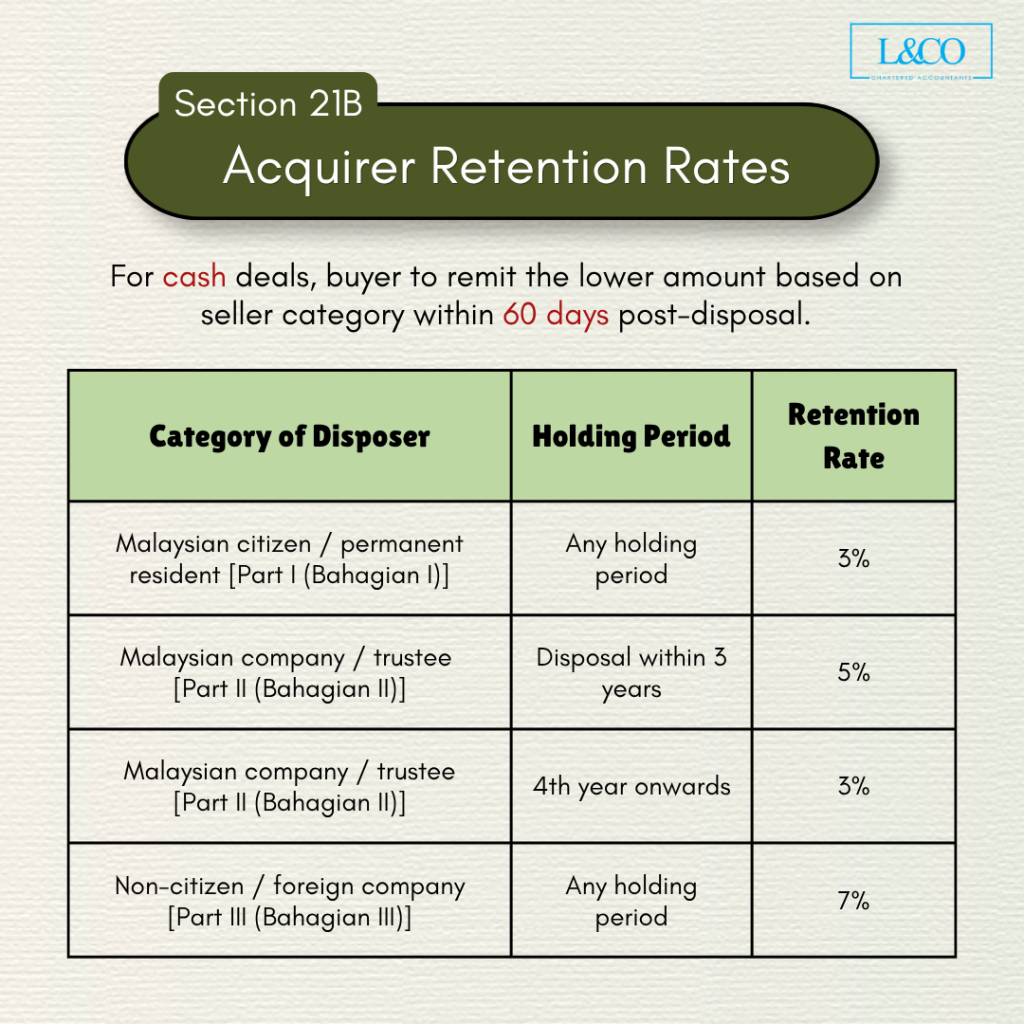

2. Acquirer Retention Rates (Section 21B)

Where the consideration for a disposal consists wholly or partly of cash, the acquirer is required to retain and remit the applicable percentage to the Director General of Inland Revenue (DGIR) within 60 days of the date of disposal.

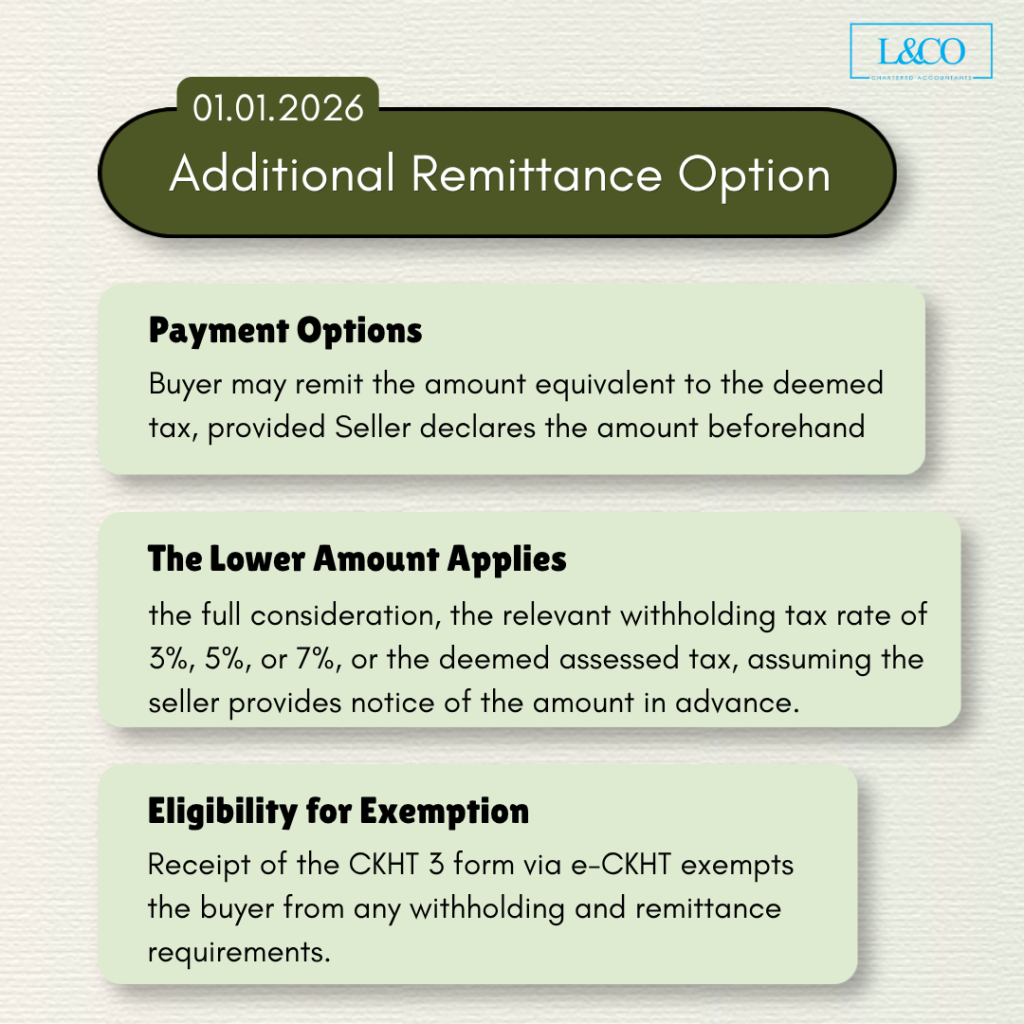

🆕 New from 1 January 2026: Additional Remittance Optio

Acquirers may now elect to remit an amount equivalent to the deemed assessed tax (where the disposer has communicated this figure prior to remittance). The amount payable is the lower of:

(i) the full cash consideration

(ii) 3%/5%/7% of the total consideration

(iii) the deemed assessed tax amount (only if notified by the disposer in advance).

Note: If the acquirer has received Form CKHT 3 from the disposer via e-CKHT on MyTax, the acquirer is exempt from the obligation to retain and remit amounts under Section 21B.

3. Responsibilities of the Acquirer

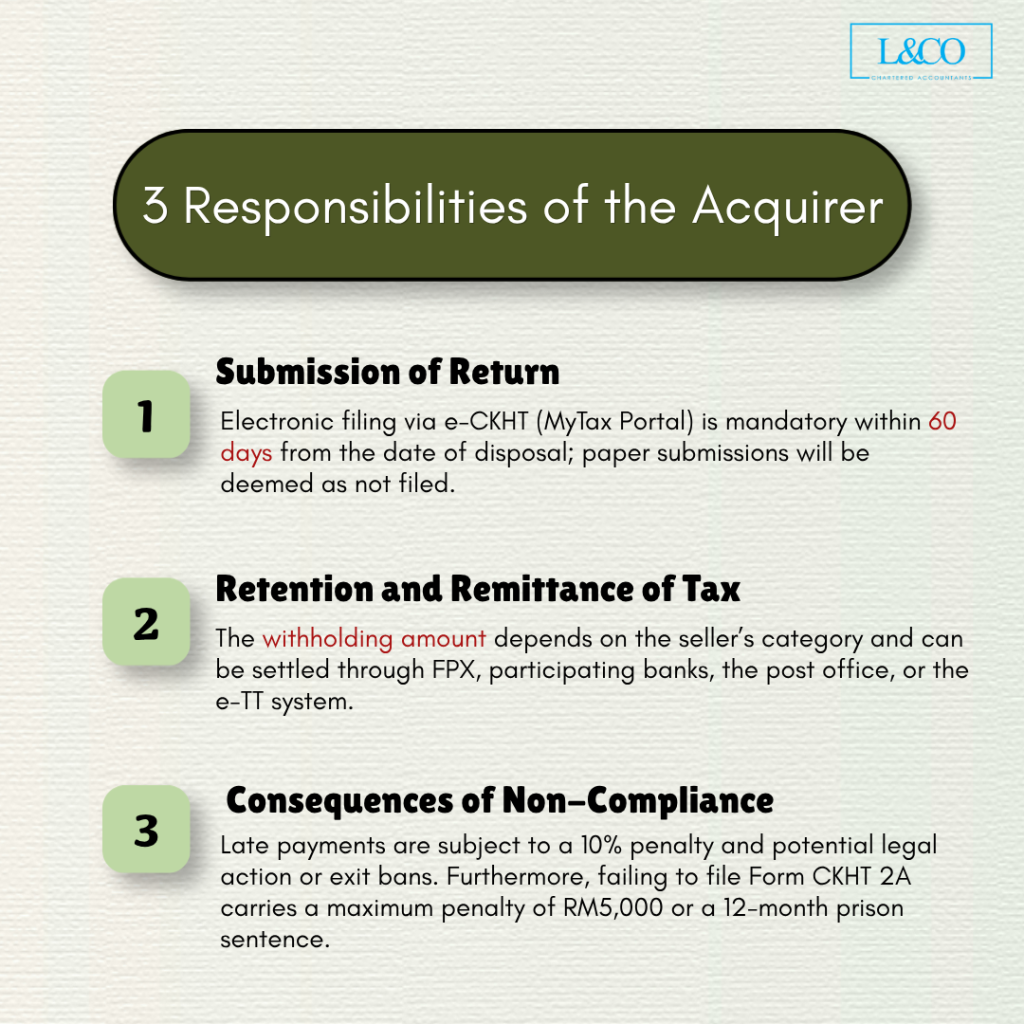

3.1 Submission of Return

- Form CKHT 2A must be submitted within 60 days of the date of acquisition.

- Electronic filing is mandatory via the e-CKHT platform on the MyTax portal: mytax.hasil.gov.my (effective 1 January 2025).

- Paper submissions are not accepted and will be treated as a failure to file unless resubmitted electronically.

- Each acquirer must file a separate Form CKHT 2A.

- Acquirers without a Tax Identification Number (TIN) must first register via the e-Daftar service on MyTax.

3.2 Retention and Remittance of Tax

- Where the transaction involves a cash consideration, the acquirer must retain the applicable percentage as set out in Section 2 above.

- Payment channels: ByrHasil FPX (online banking), appointed HASiL collection bank counters, Pos Malaysia (cash), or via e-TT system using a VA number generated from the Bill Number.

- The Bill Number (Nombor Bil) shown on the CKHT 2A acknowledgement slip must be used to effect payment.

3.3 Consequences of Non-Compliance

- Late remittance (beyond 60 days): A surcharge of 10% of the outstanding amount will be imposed under subsection 21B(2).

- Civil proceedings: Unpaid tax arrears become a debt due to the Government and may be recovered through civil action under Section 23.

- Travel restriction: An acquirer who fails to settle outstanding tax may be subject to an overseas travel ban under Section 22.

- Failure to file CKHT 2A: Upon conviction under subsection 29(1), a fine not exceeding RM5,000 or imprisonment not exceeding 12 months, or both.

4. Responsibilities of the Disposer

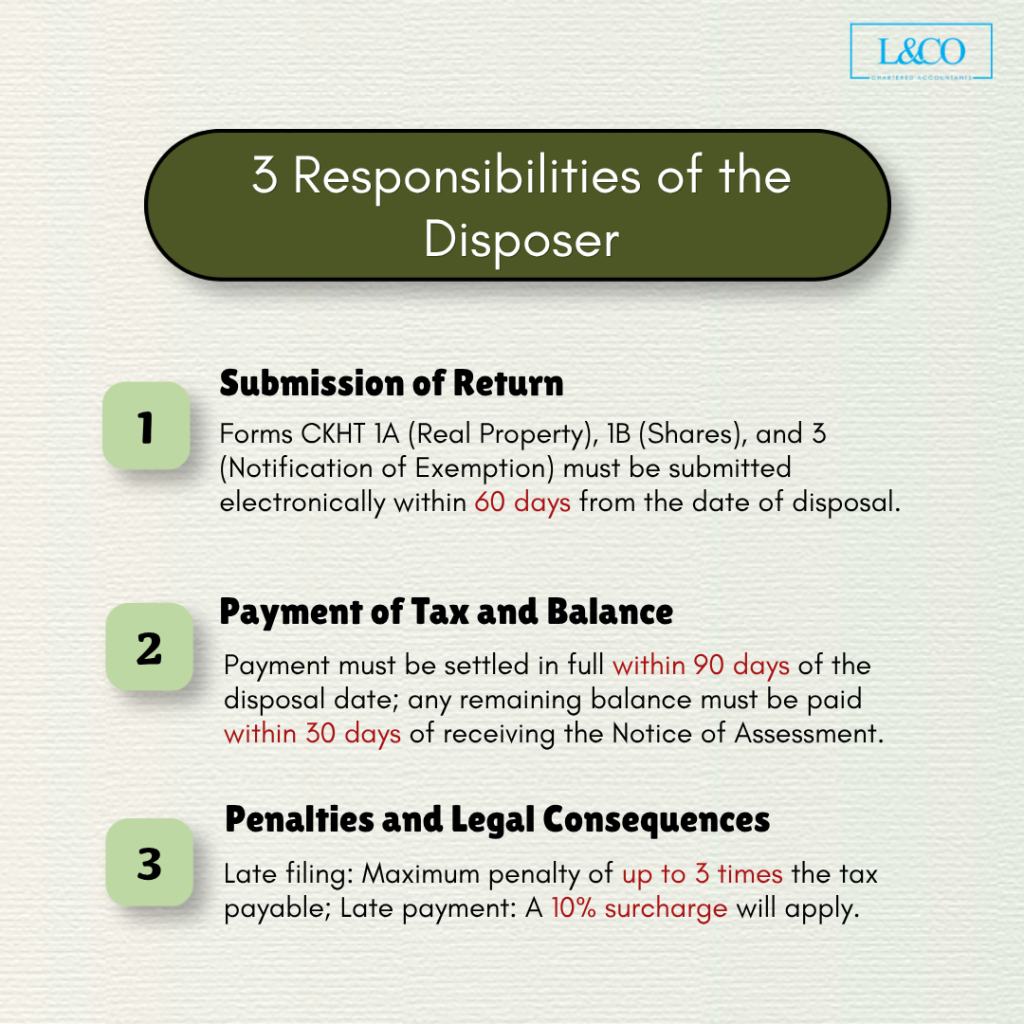

4.1 Submission of Return

| Form | Applicable Scenario |

| CKHT 1A | Disposal of real property chargeable under the Real Property Gains Tax Act 1976 (RPGTA 1976) |

| CKHT 1B | Disposal of shares chargeable under paragraphs 34 or 34A of Schedule 2, RPGTA 1976 |

| CKHT 3 | Notification under subsection 13(6) RPGTA 1976 — certifying that the disposal is not chargeable or is exempt from tax |

- Deadline: Within 60 days of the date of disposal; electronic submission via e-CKHT is mandatory.

- Self-Assessment System (STS) from 2025: A BNCKHT filed under Section 13 is treated as a notice of assessment, deemed served on the date of filing.

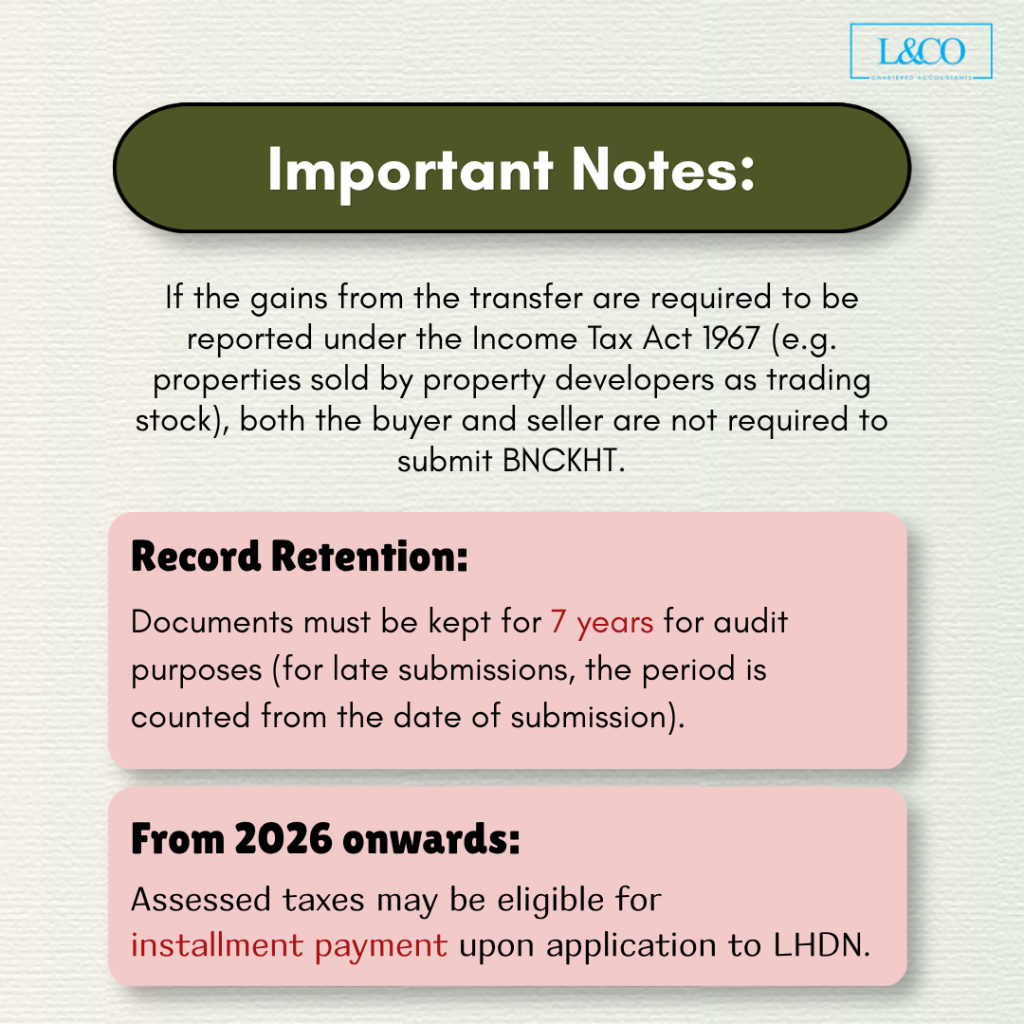

- All supporting records must be retained for seven (7) years from the end of the year of assessment (or, where filing was late, from the end of the year in which the return was filed).

4.2 Payment of Tax and Balance

- 90-day payment rule: Tax payable under a deemed assessment must be settled within 90 days of the date of disposal, irrespective of any appeal.

- Where the amount remitted by the acquirer under Section 21B is less than the total tax liability, the disposer is responsible for settling the shortfall.

- 30-day rule for assessment notices: Where an original or additional assessment notice is issued, the balance must be paid within 30 days of that notice.

- Instalment option from 1 January 2026: Tax payable under a deemed assessment may be paid by instalments, subject to the amount and schedule approved by the DGIR.

4.3 Penalties and Legal Consequences

- Late filing (beyond 60 days): A penalty of up to three (3) times the tax payable may be imposed under subsection 29(3).

- Late payment (beyond 90 days): A surcharge of 10% of the tax or balance tax due will be imposed under subsection 21(4).

- Incorrect information: A penalty equivalent to the amount of tax undercharged may be imposed under subsection 30(2).

- Erroneous CKHT 3 notification: Where an incorrect notification causes the acquirer to fail to remit the required amount, an additional charge of 10% of the tax payable will be included in the assessment (subsections 14(5) and 15(4)).

- Civil proceedings and travel restrictions may also be imposed — same provisions as those applicable to the acquirer (Sections 22 and 23).

5. Mandatory Electronic Filing — e-CKHT

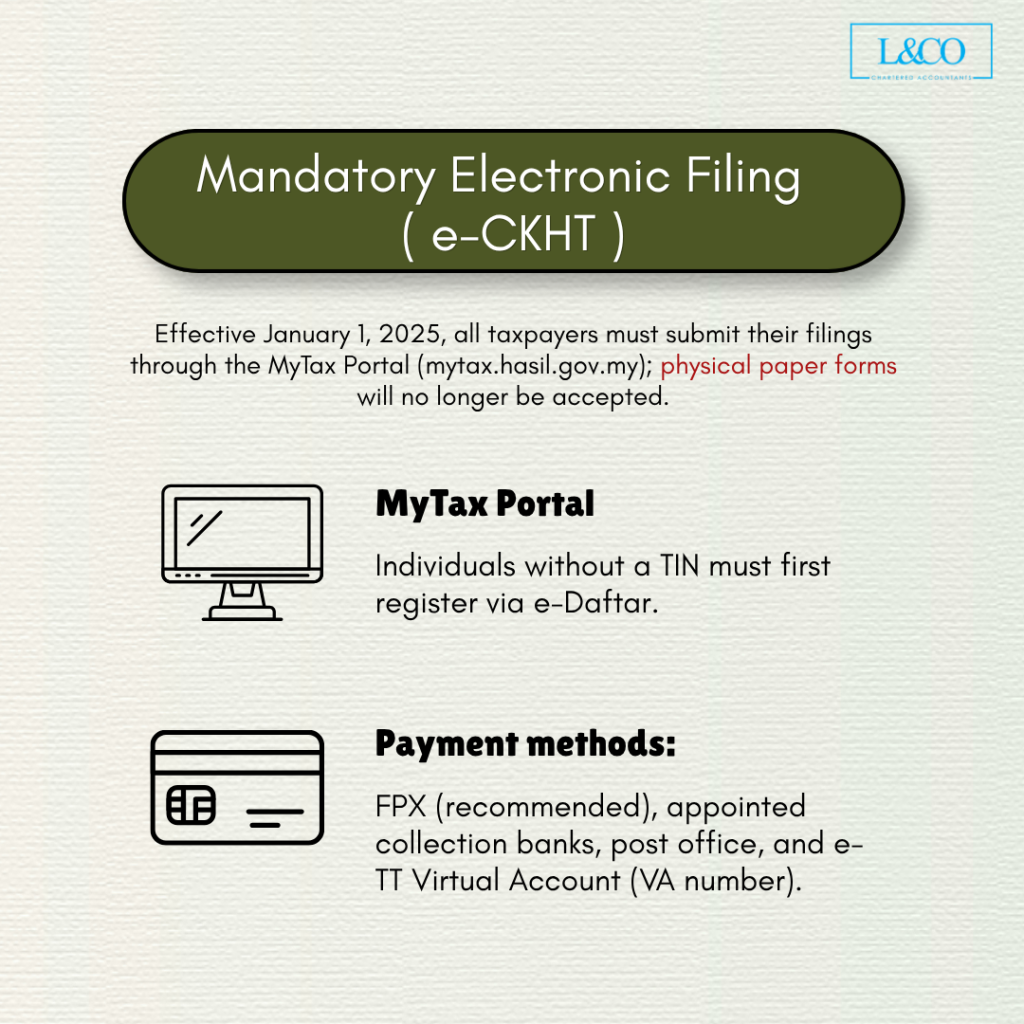

⚠️ Mandatory Requirement Effective 1 January 2025

All taxpayers — both acquirers and disposers — are required to submit returns through the MyTax portal (mytax.hasil.gov.my) via the e-CKHT platform. Physical / paper submissions will no longer be accepted and will be treated as a failure to file.

- Completion notes and user guides for e-CKHT are available for download at: LHDN Official Portal > Download Forms > CKHT.

- Taxpayers without a Tax Identification Number (TIN) must register via the e-Daftar service on MyTax prior to filing.

- Sample BNCKHT forms may also be downloaded and printed from the same portal.

Authorised Payment Channels

| Payment Channel | Details |

| ByrHasil FPX (Recommended) | Online payment via byrhasil.hasil.gov.my; the taxpayer must hold an internet banking account with any participating FPX member bank. |

| HASiL Collection Bank Counter | Payment at any appointed HASiL collection bank using the Bill Number (Nombor Bil) only. |

| Pos Malaysia Office | Cash payment accepted at any Pos Malaysia counter. |

| e-TT System (VA Number) | Generate a Virtual Account (VA) number from the e-TT system using the Bill Number and effect a bank transfer. |

6. Tax Refund Procedures

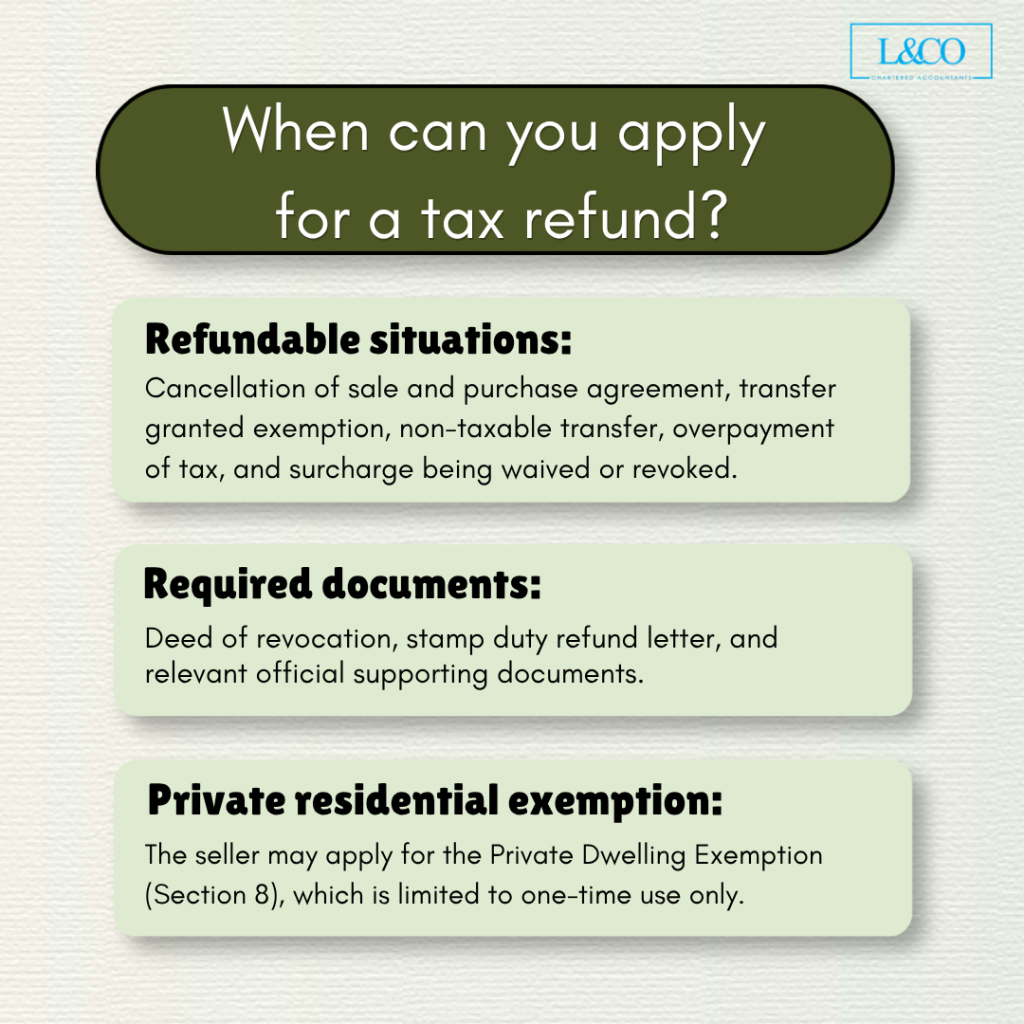

6.1 Circumstances Giving Rise to a Refund

- The sale and purchase agreement is rescinded or cancelled.

- The disposal qualifies for a tax exemption.

- The disposal is not chargeable to tax.

- Tax has been overpaid.

- A surcharge has been remitted or waived.

6.2 Documents Required for a Refund Application

- Deed of Revocation or instrument of cancellation of the disposal; or

- Letter confirming stamp duty refund, together with supporting documents; or

- Any other official document evidencing the cancellation of the disposal or transaction.

⚠️ Important: Refund Principles

Tax refunds are, as a matter of law, payable to the disposer, as the tax is charged on the disposer’s gains. Where a refund is to be directed to the acquirer instead, the disposer must execute a Consent Letter (in the form prescribed under Lampiran 1), duly affirmed before a Commissioner for Oaths, and submit it to the relevant LHDN State Office or Special Branch handling the disposer’s file.

7. Exemptions

7.1 Transactions Not Requiring BNCKHT Submission

- Where the gains from a disposal are chargeable to tax under the Income Tax Act 1967 (ITA 1967) rather than the RPGTA 1976, neither party is required to submit a BNCKHT.

- Example: A property developer selling houses to purchasers — the properties constitute trading stock of the developer, and any profit is assessed under ITA 1967, not RPGT.

7.2 Private Residence Exemption

- Eligibility: A disposer may elect to claim a RPGT exemption on the disposal of a private residence under Section 8, RPGTA 1976.

- Application is made via Form CKHT 3 (Lampiran 3 may be completed electronically at mytax.hasil.gov.my).

- Important: This exemption may only be utilised once in a lifetime.

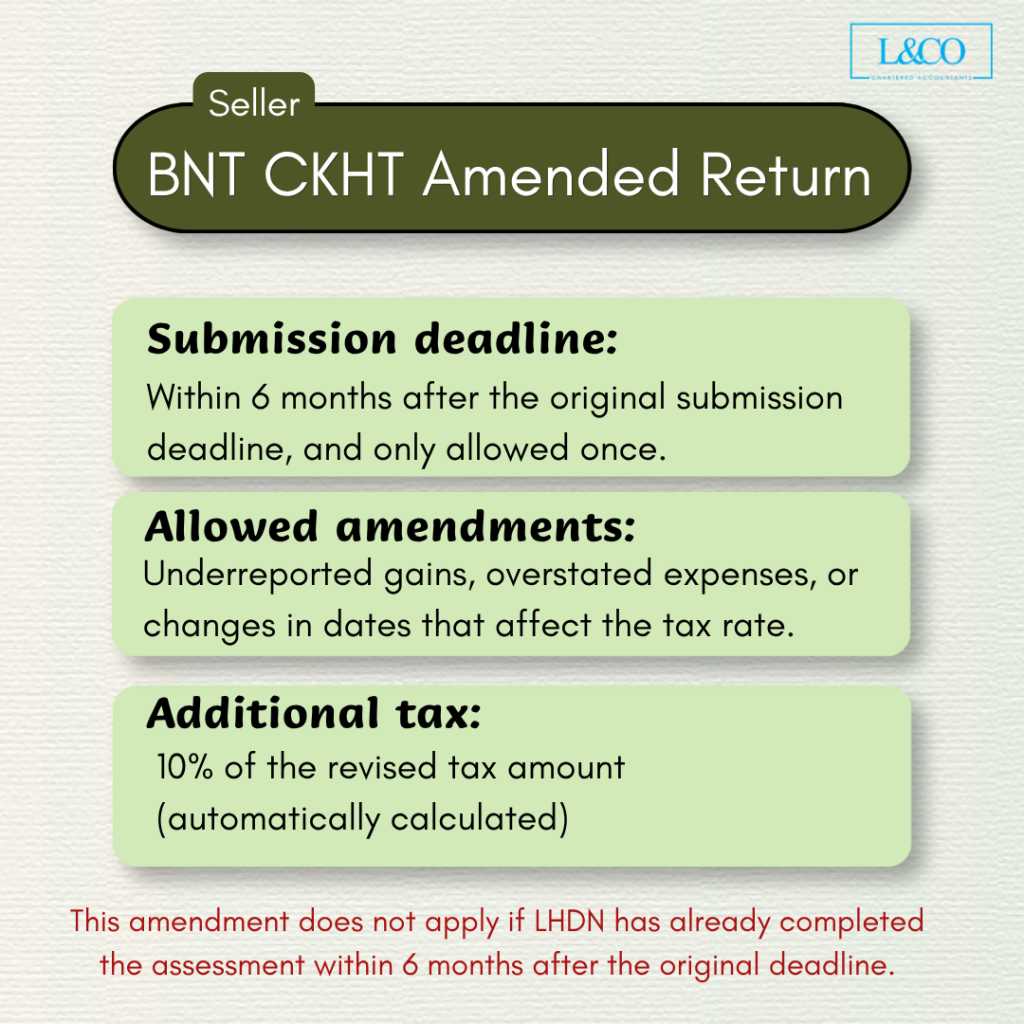

8. Amended Return (BNT CKHT)

Pursuant to the new Section 13A of the RPGTA 1976 (in force from 1 January 2025), a disposer who has filed a BNCKHT within the prescribed period may make one self-amendment to the deemed assessment, subject to the eligibility criteria below.

| Item | Details |

| Filing deadline | Within 6 months of the original prescribed filing deadline (i.e., 60 days after the date of disposal) |

| Number of amendments | Once only |

| Permitted grounds | Under-reported or omitted gains; over-claimed incidental costs; change in date of disposal or acquisition affecting the applicable tax rate |

| Not eligible | Where the DGIR has already raised an assessment for that year of assessment within the 6-month window |

| Surcharge on amendment | 10% of the additional tax payable arising from the amendment (calculated automatically) |

| Applicable forms | BNT CKHT 1A (real property disposal) or BNT CKHT 1B (share disposal) |

**Information updated on 01.04.2026