e-Invoice means recording every transaction electronically. With the full implementation of e-Invoice, we will no longer need to keep physical receipts and all transaction records will be backed up in the LHDN database.

Malaysia e-Invoice will be fully implemented soon. Are you ready? Don’t worry, this guideline will highlight for you the most important points in the simplest words!

Frequent Asked Questions

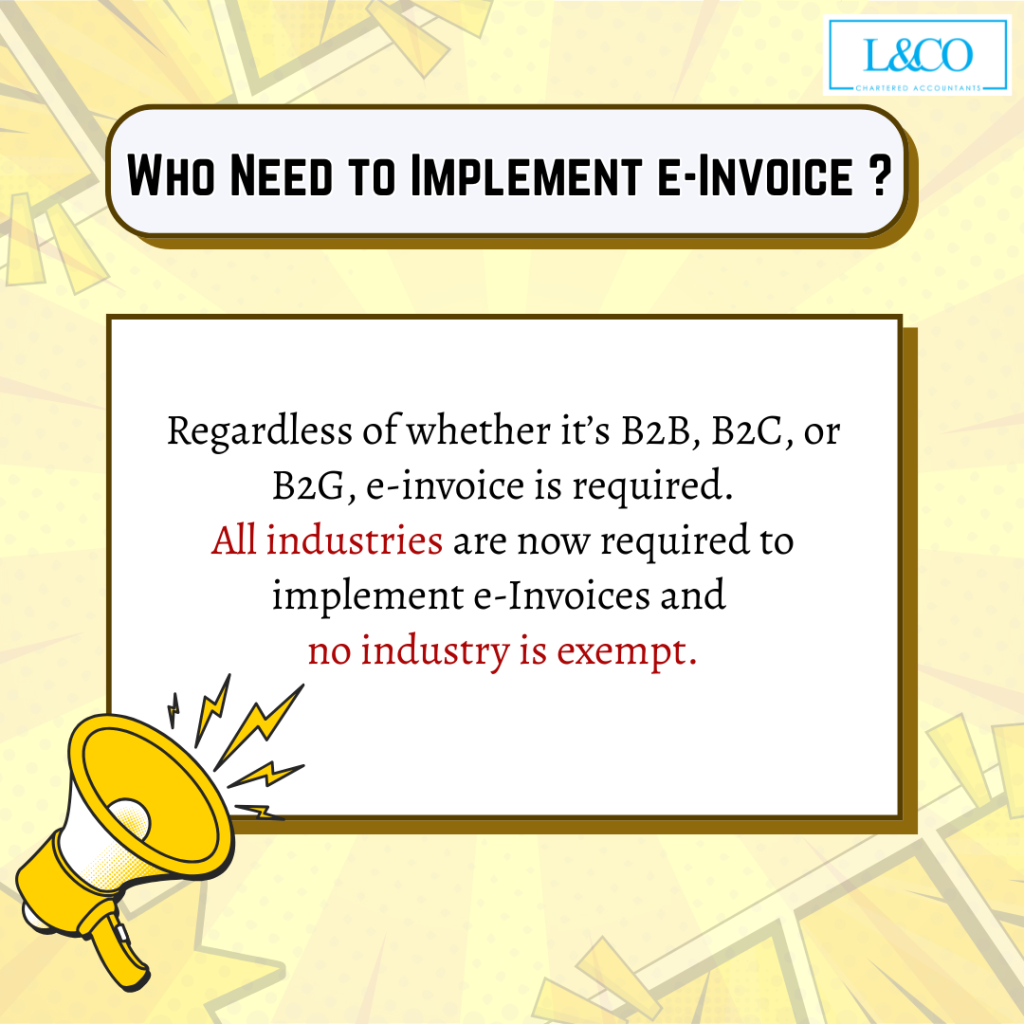

Regardless of whether it’s B2B, B2C, or B2G, e-invoice is required. All industries are now required to implement e-Invoices and no industry is exempt.

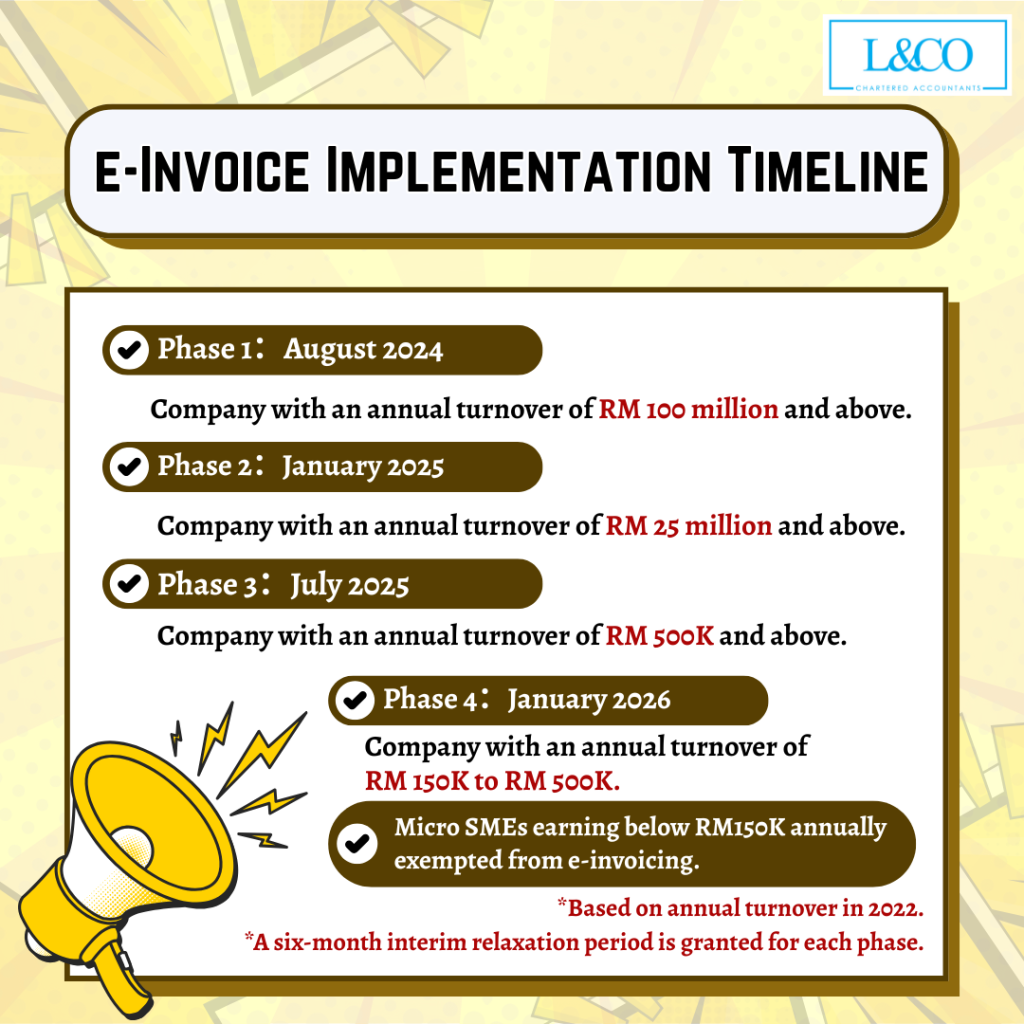

- Phase 1:August 2024

Company with an annual turnover of RM 100 million and above.

. - Phase 2:January 2025

Company with an annual turnover of RM 25 million and above.

. - Phase 3:July 2025

Company with an annual turnover of RM 500K and above.

. - Phase 4:January 2026

Company with an annual turnover of RM 150K to RM 500K.

. - Micro SMEs earning below RM150K annually exempted from e-Invoicing.

*𝐁𝐚𝐬𝐞𝐝 𝐨𝐧 𝐚𝐧𝐧𝐮𝐚𝐥 𝐭𝐮𝐫𝐧𝐨𝐯𝐞𝐫 𝐢𝐧 𝟐𝟎𝟐𝟐.

*𝐀 𝐬𝐢𝐱-𝐦𝐨𝐧𝐭𝐡 𝐢𝐧𝐭𝐞𝐫𝐢𝐦 𝐫𝐞𝐥𝐚𝐱𝐚𝐭𝐢𝐨𝐧 𝐩𝐞𝐫𝐢𝐨𝐝 𝐢𝐬 𝐠𝐫𝐚𝐧𝐭𝐞𝐝 𝐟𝐨𝐫 𝐞𝐚𝐜𝐡 𝐩𝐡𝐚𝐬𝐞.

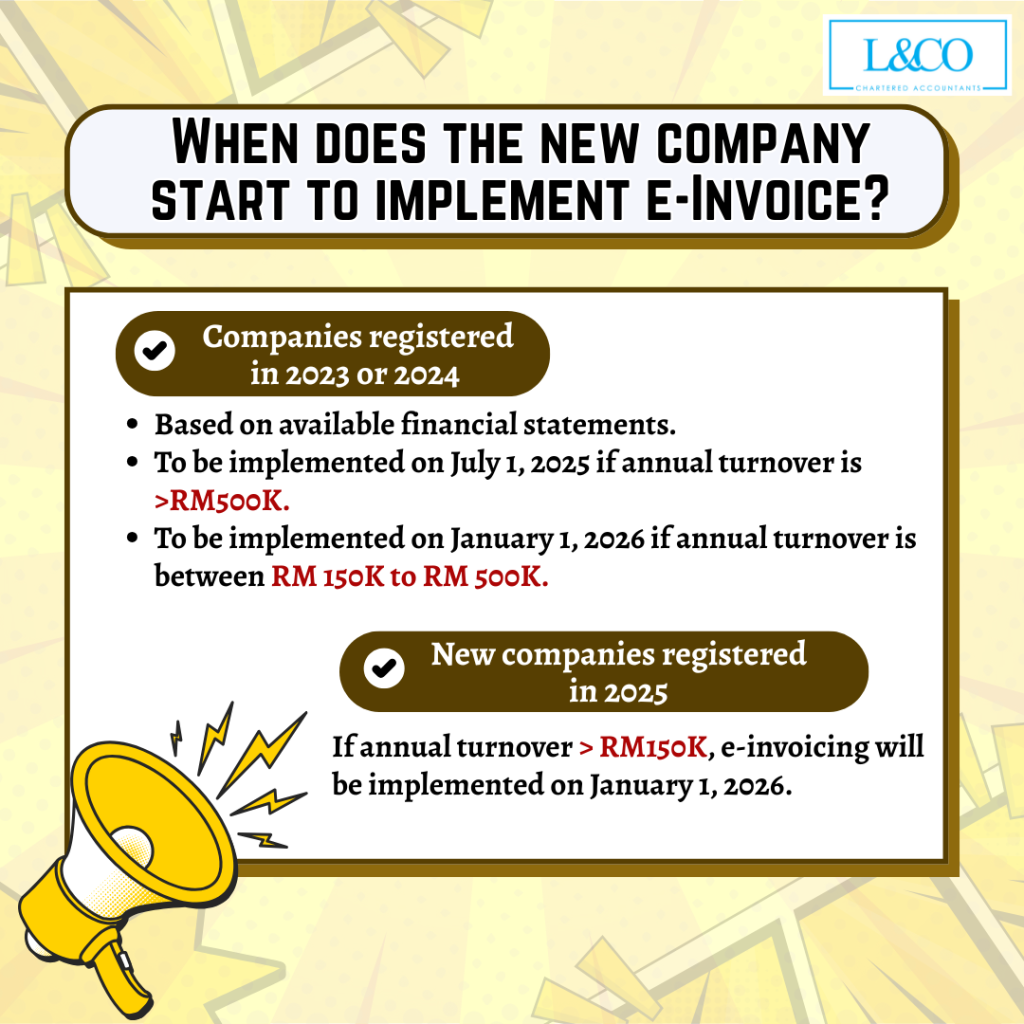

- Companies registered in 2023 or 2024

– Based on available financial statements.

– To be implemented on July 1, 2025 if annual turnover > RM500K.

– To be implemented on January 1, 2026 if annual turnover is between RM 150K to RM 500K.

- New companies registered in 2025

– If annual turnover > RM150K, e-invoicing will be implemented on January 1, 2026.

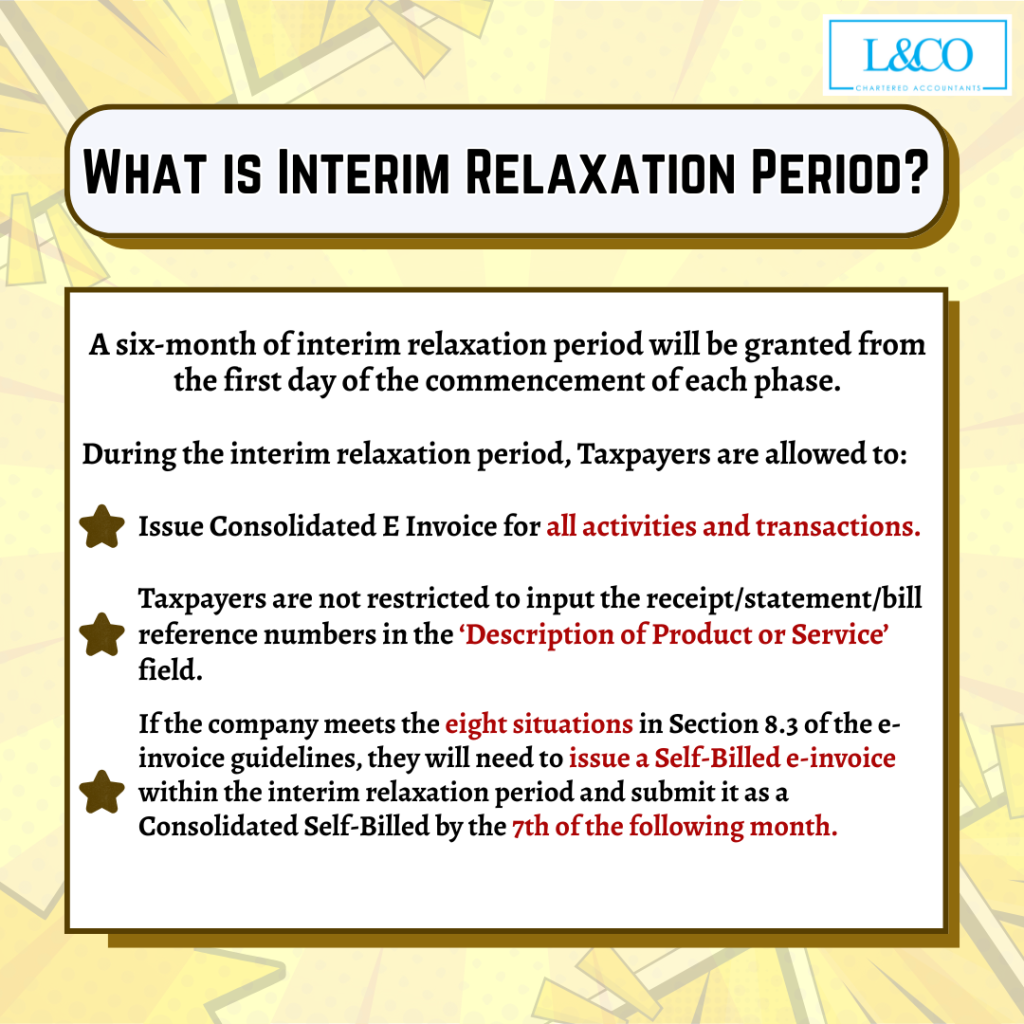

- A six-month of interim relaxation period will be granted from the first day of the commencement of each phase.

- During the interim relaxation period, Taxpayers are allowed to:

– Issue Consolidated E Invoice for all activities and transactions.

– Taxpayers are not restricted to input the receipt/statement/bill reference numbers in the ‘Description of Product or Service’ field.

– If the company meets the eight situation in Section 8.3 of the e-invoice guidelines, they will need to issue a Self-Billed e-invoice within the interim relaxation period and submit it as a Consolidated Self-Billed by the 7th of the following month.

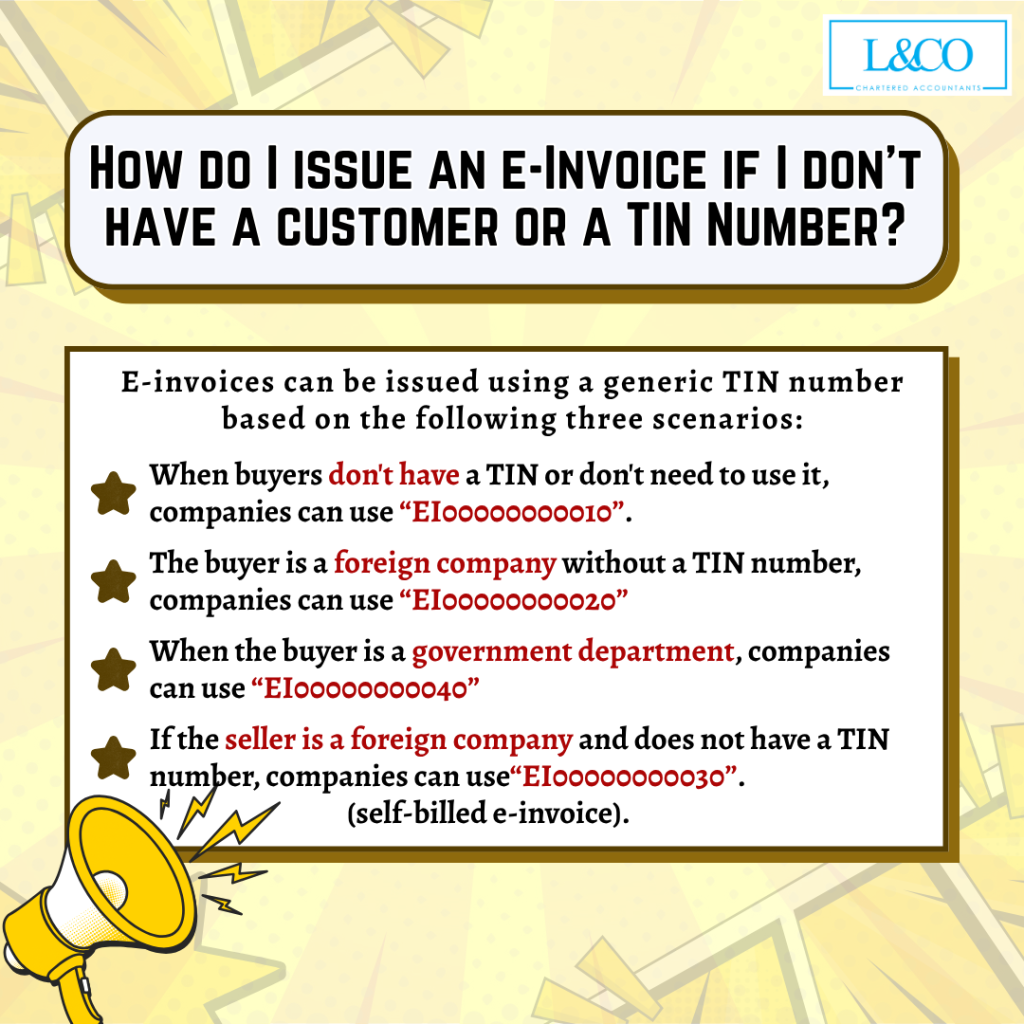

e-Invoices can be issued using a generic TIN number based on the following three scenarios:

- When buyers don’t have a TIN or don’t need to use it, companies can use “EI00000000010”.

- The buyer is a foreign company without a TIN number, companies can use “EI00000000020”.

- When the buyer is a government department, companies can use “EI00000000040”.

- If the seller is a foreign company and does not have a TIN number, companies can use “EI00000000030” (self-billed e-invoice).

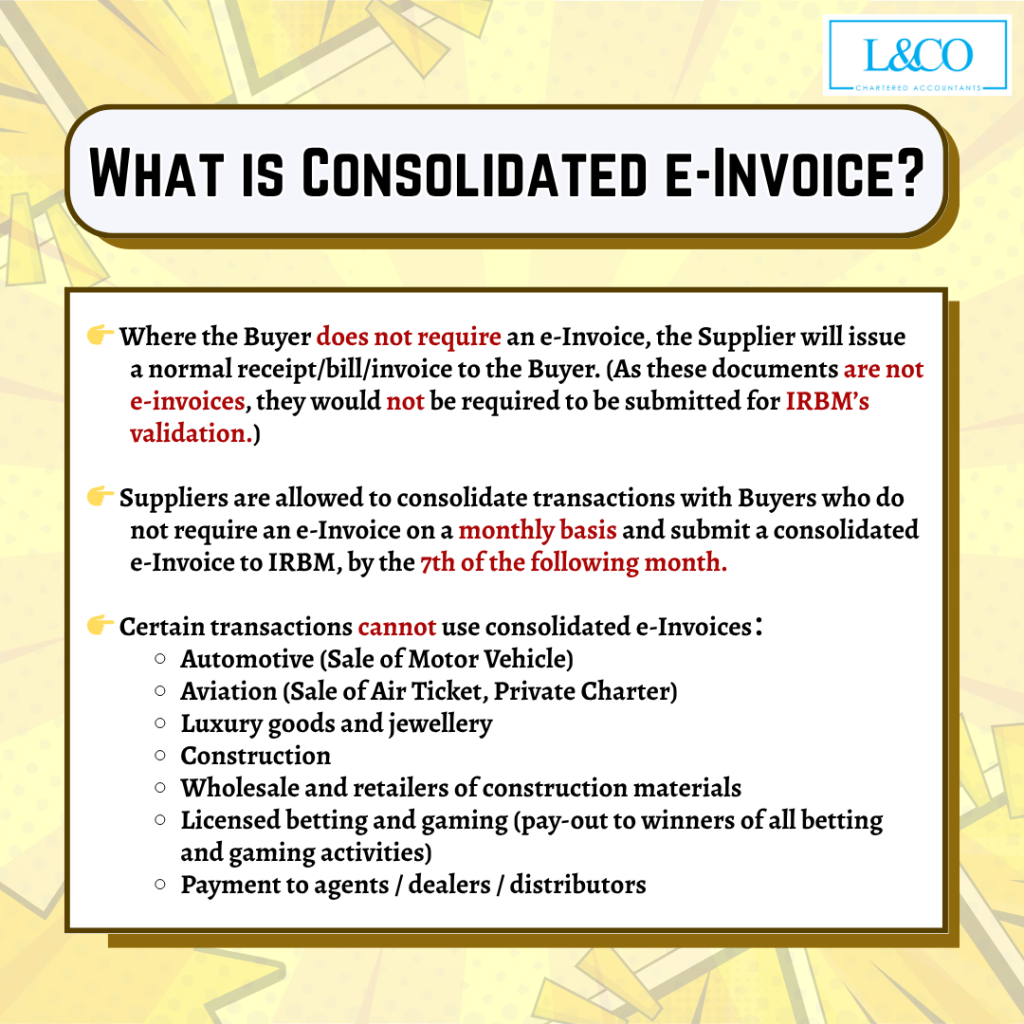

- Where the Buyer does not require an e-Invoice, the Supplier will issue a normal receipt/bill/invoice to the Buyer. (As these documents are not e-invoices, they would not be required to be submitted for IRBM’s validation).

- Suppliers are allowed to consolidate transactions with Buyers who do not require an e-Invoice on a monthly basis and submit a consolidated e-Invoice to IRBM, by the 7th of the following month.

- Certain transactions cannot use consolidated e-invoices:

– Automotive (Sale of Motor Vehicle)

– Aviation (Sale of Air Ticket, Private Charter)

– Luxury goods and jewellery

– Construction (Contract as defined in ITA 1967)

– Wholesale and retailers of construction materials (Defined in Lembaga Pembangunan Industri Pembinaan Malaysia Act 1994)

– Licensed betting and gaming (pay-out to winners of all betting and gaming activities) (Casino and gaming machines are exempted until further notice, as per e-invoice specific guide issued by LHDN on 28 Oct 23)

– Payment to agents / dealers / distributors (defined in ITA 1967)

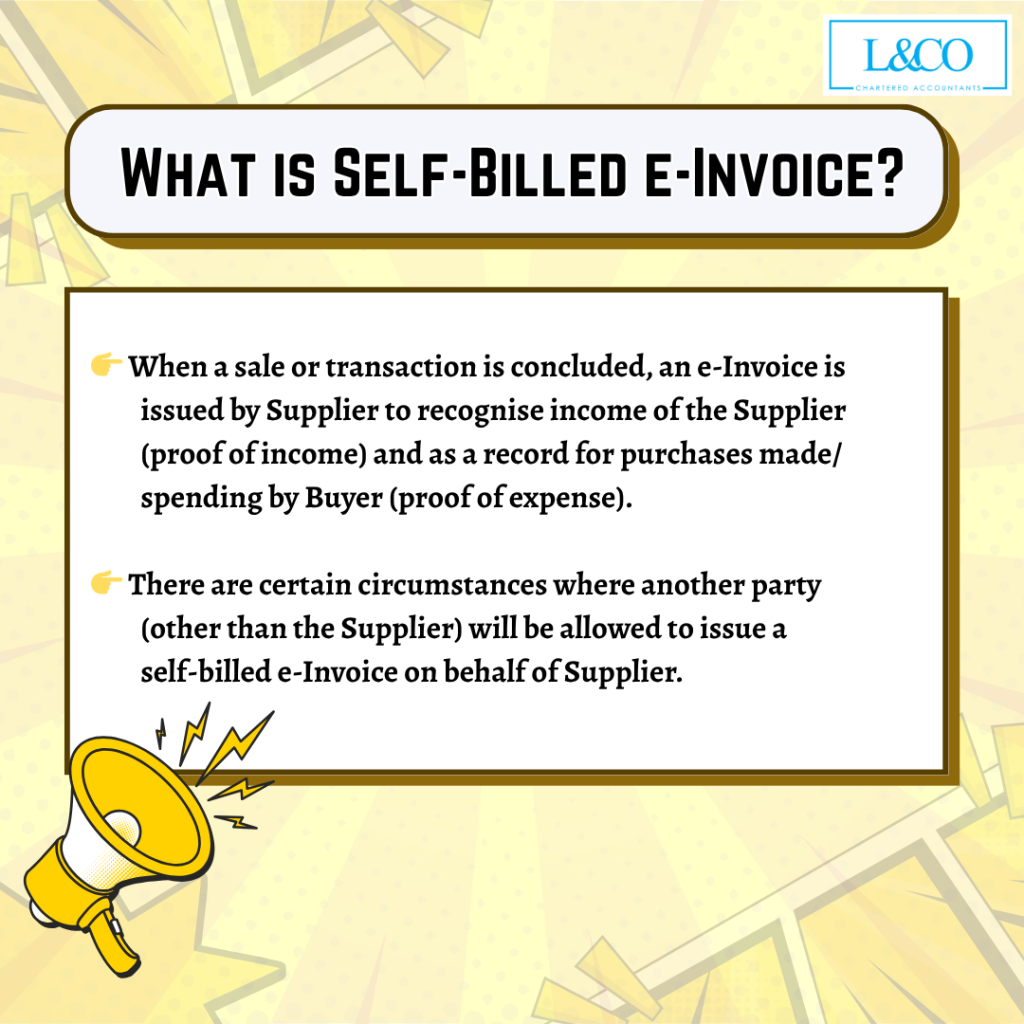

- When a sale or transaction is concluded, an e-Invoice is issued by Supplier to recognise income of the Supplier (proof of income) and as a record for purchases made/ spending by Buyer (proof of expense).

- There are certain circumstances where another party (other than the Supplier) will be allowed to issue a self-billed e-Invoice on behalf of Supplier.

- Payment to agents, dealers, distributors, etc.

- Goods sold or services rendered by foreign suppliers

- Profit distribution (e.g., dividend distribution)

- e-Commerce transactions

- Pay-out to all betting and gaming winners

- Acquisition of goods or services from individual taxpayers

- Interest

- Insurance Compensation

- Capital reduction / share buybacks

- Rent, property management & staff training costs

*Updated on 14.05.2025