With the implementation of e-Invoicing, many businesses are uncertain whether self-billing is applicable in specific situations.

The answer largely depends on the nature of the supplier and the transaction.

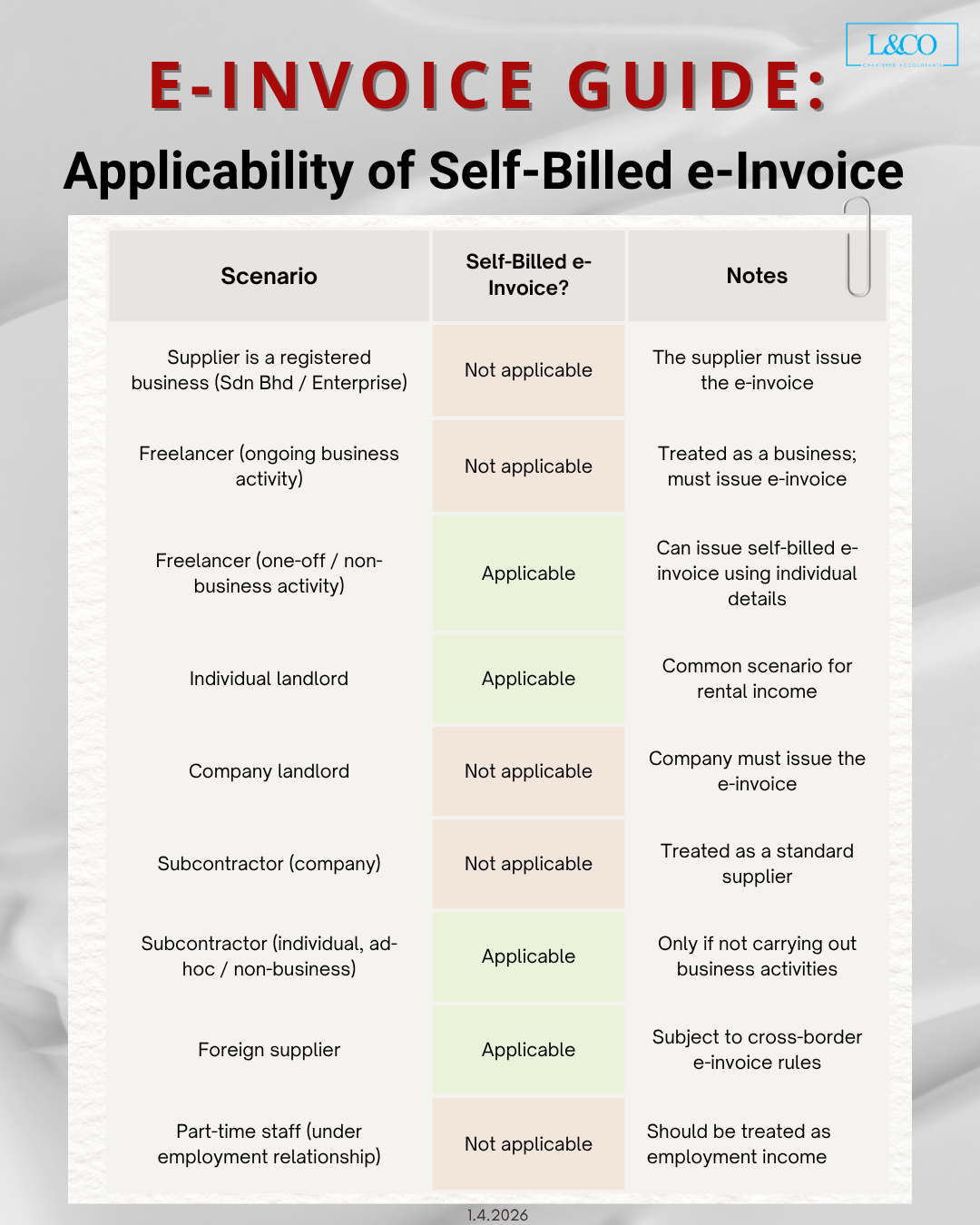

The primary consideration is: Whether the supplier is carrying on a business activity

When Self-Billing is NOT Applicable

Self-billing is generally not allowed when dealing with:

- Registered businesses (Sdn Bhd / Enterprise)

- Freelancers with ongoing business activities

- Company-owned rental arrangements

- Corporate subcontractors

When Self-Billing is Applicable

Self-billing may be used when dealing with:

- Individuals earning one-off or non-recurring income

- Individual landlords (non-business)

- Temporary or ad-hoc individual service providers

Special Considerations

Certain transactions require additional assessment:

- Foreign suppliers: subject to cross-border tax rules

- Employees / staff claims: treated as payroll, not self-billing

Conclusion

The applicability of self-billing depends on distinguishing between:

- Business transactions

- Non-business individual transactions

Businesses should evaluate each case carefully to ensure compliance with tax regulations.

**Data Updated on 01.04.2026