In business operations, overdue customer payments are a common financial risk. When a company determines that a receivable can no longer be collected, it is classified as a Bad Debt, and proper accounting treatment is required to ensure accurate financial reporting and tax compliance.

This guide explains what bad debts are, how they are identified, the role of bad debt provisions, and the proper accounting treatment.

What is a Bad Debt?

A Bad Debt refers to an accounts receivable (Trade Receivable) that a company has confirmed is no longer recoverable from a customer.

From an accounting perspective, bad debt is considered an impairment of assets. A receivable that was originally recorded as an asset in the Balance Sheet must be transferred to the Profit & Loss (P&L) / Income Statement as an expense once it is confirmed to be uncollectible.

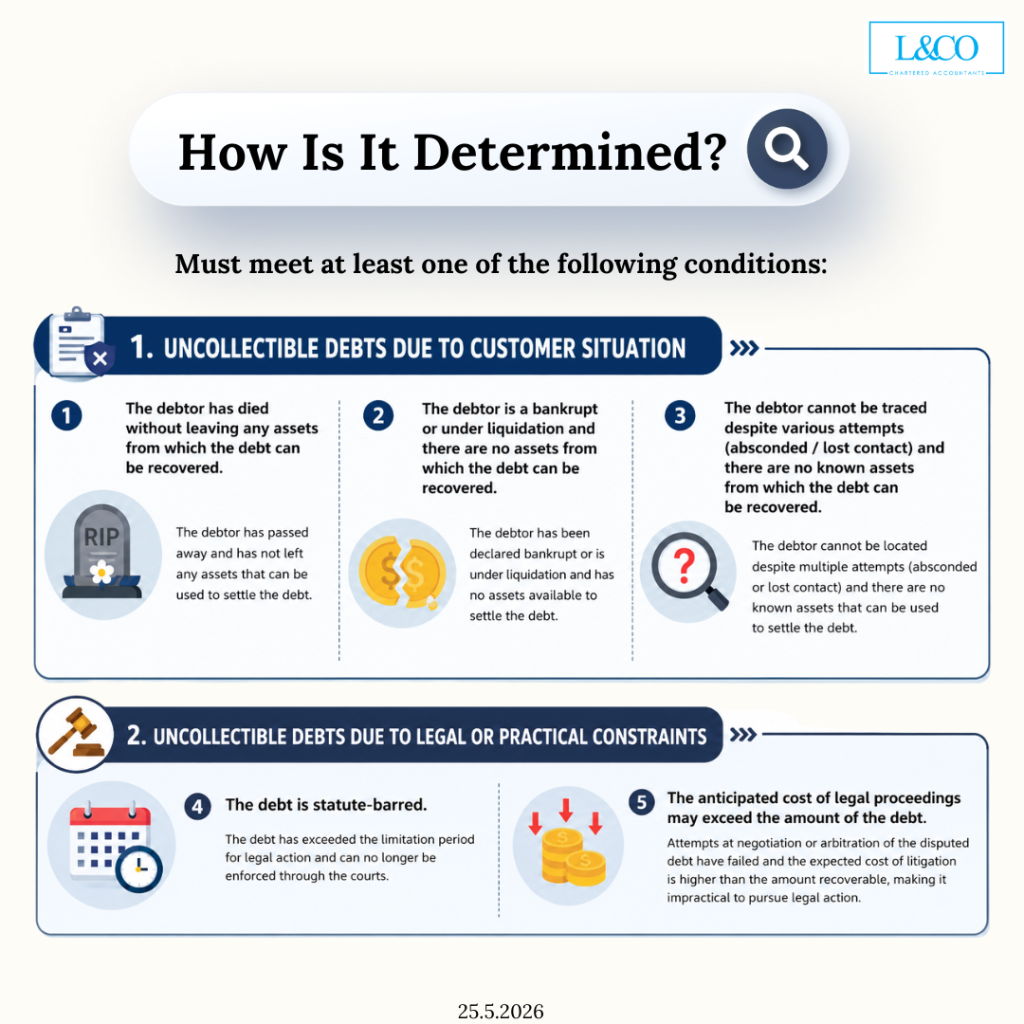

How is a Bad Debt Identified?

A debt is not automatically considered bad simply because a customer pays late. There must be reasonable evidence to support the classification.

Generally, a debt may be treated as bad if it meets one of the following conditions:

1. Debts That Cannot Be Recovered Due to Objective Circumstances

Examples include:

- The debtor has passed away and left no assets to settle the debt

- The debtor is bankrupt or the company is under liquidation with no assets available for repayment

- The debtor cannot be traced despite repeated collection efforts, and there are no known assets available

2. Debts That Cannot Be Recovered Due to Legal or Practical Reasons

Examples include:

- The debt has exceeded the legal recovery period (statute-barred debt)

- The legal or recovery cost is higher than the debt itself, making recovery uneconomical

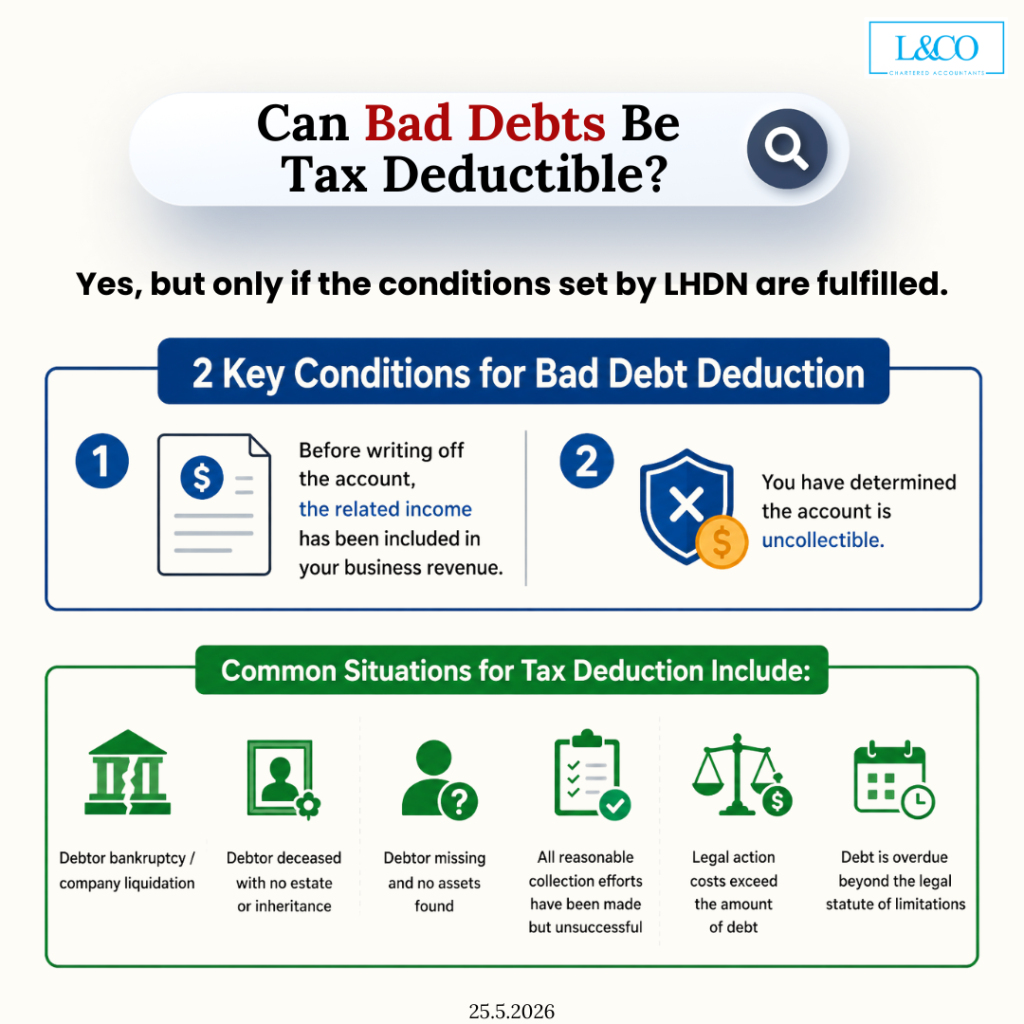

Can Bad Debt Be Tax Deductible?

Yes, but only if certain conditions are met.

To qualify for a tax deduction, bad debts generally must satisfy the following 2 basic conditions:

1. The debt was previously included in business income

This means the sales or service income had already been recognized as part of the company’s taxable business income.

2. The debt is confirmed to be unrecoverable

The company must have reasonable evidence proving the debt cannot be recovered, rather than merely being overdue.

Common Tax-Deductible Situations Include:

- Debtor is bankrupt / company under liquidation

- Debtor has passed away with no estate left behind

- Debtor cannot be traced and has no known assets

- Reasonable recovery actions were taken but collection failed

- Legal costs are higher than the debt amount

- The debt has exceeded the legal recovery limitation period

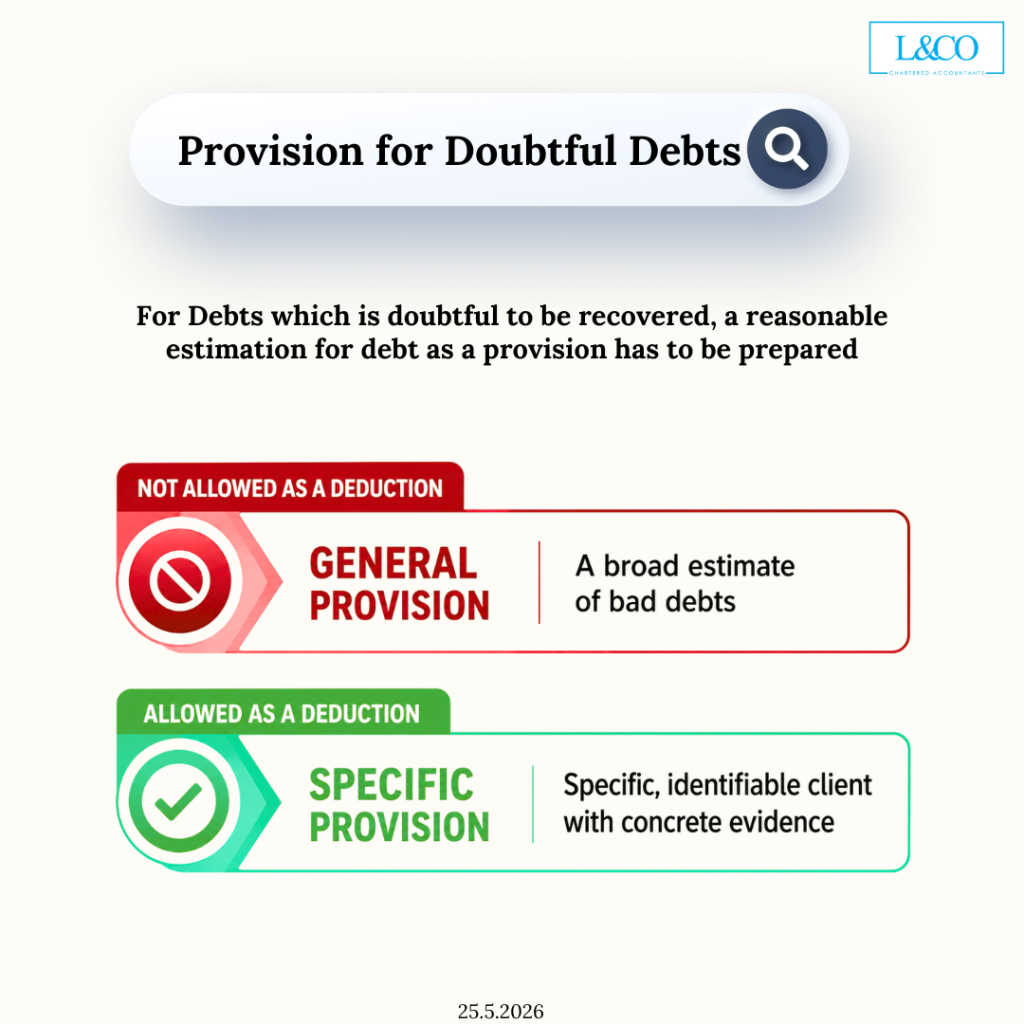

What is Provision for Bad Debts?

If a company believes that certain receivables may become uncollectible but there is not yet sufficient evidence to confirm them as bad debts, it will usually record a Provision for Bad Debts first.

This is a precautionary accounting treatment used to reflect potential losses in advance.

General Provision for Bad Debts

This refers to an estimated provision made based on a percentage of receivables, for example:

2% or 5% of total receivables estimated as potentially uncollectible

Characteristics:

- Based on estimation

- No specific debtor identified

- Generally not tax deductible

Specific Provision for Bad Debts

This refers to a provision made for a specific receivable where there is clear evidence of collection risk, such as:

- Long overdue debts

- Legal demand letters issued

- Customer bankruptcy or liquidation

- Supporting evidence showing the debt is unlikely to be recovered

Characteristics:

- Specific debtor identified

- Supported by evidence

- May qualify for tax deduction subject to conditions

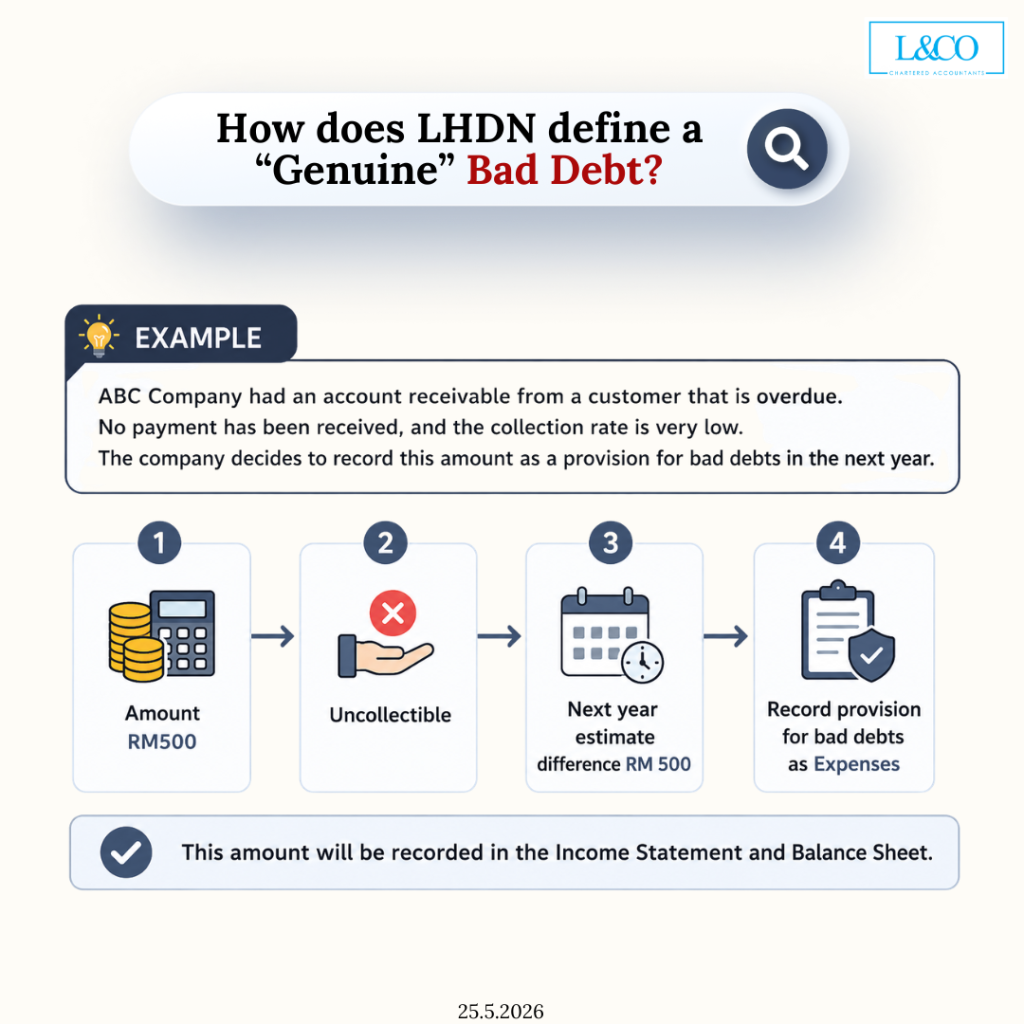

How is a Bad Debt Provision Adjusted?

Assume:

ABC Company has an RM500 receivable that has remained unpaid beyond the due date.

After repeated follow-ups, management believes the likelihood of recovery is very low.

Before officially writing it off, the company may:

Record a RM500 provision for bad debts

Financial impact:

- Income Statement – Recorded as an expense

- Balance Sheet – Reduces the net recoverable value of receivables

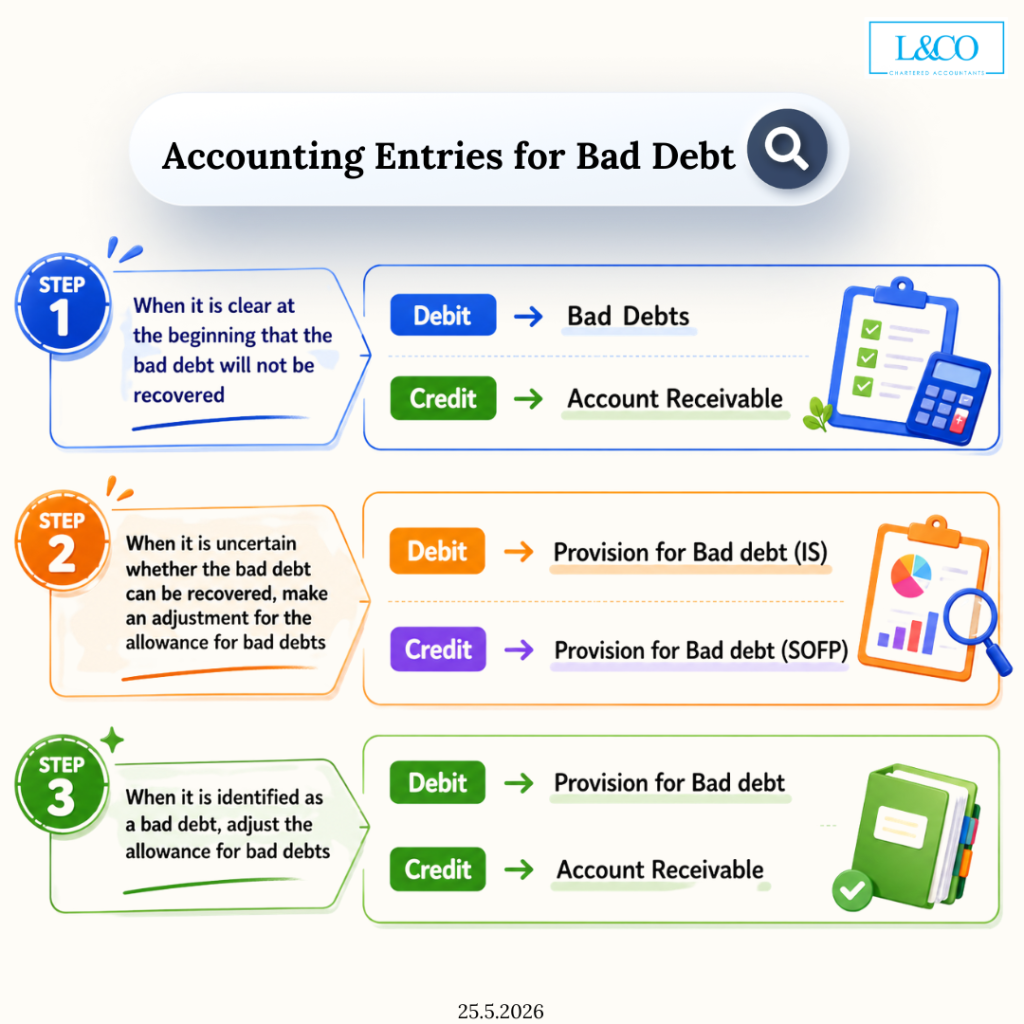

If the debt is later confirmed to be uncollectible, it will then be written off as bad debt.

Why is Timely Bad Debt Treatment Important?

Failing to manage bad debts properly may result in:

- Inaccurate financial statements

- Overstated receivables

- Inflated profits

- Incorrect tax treatment

- Poor management decision-making

Regular review of receivables helps companies reflect their true financial position.