The Malaysian Government has introduced the New Incentive Framework (NIF), a revamped investment incentive system designed to attract high-value investments through a more transparent outcome-based incentive approach. The framework aims to accelerate industrial upgrading, economic transformation, and sustainable growth.

Unlike the previous incentive system, which primarily focused on industry classification, the NIF emphasizes a company’s long-term contribution to Malaysia’s economy. Key assessment areas include innovation, high-value employment, local supply chain development, sustainability, and overall economic impact.

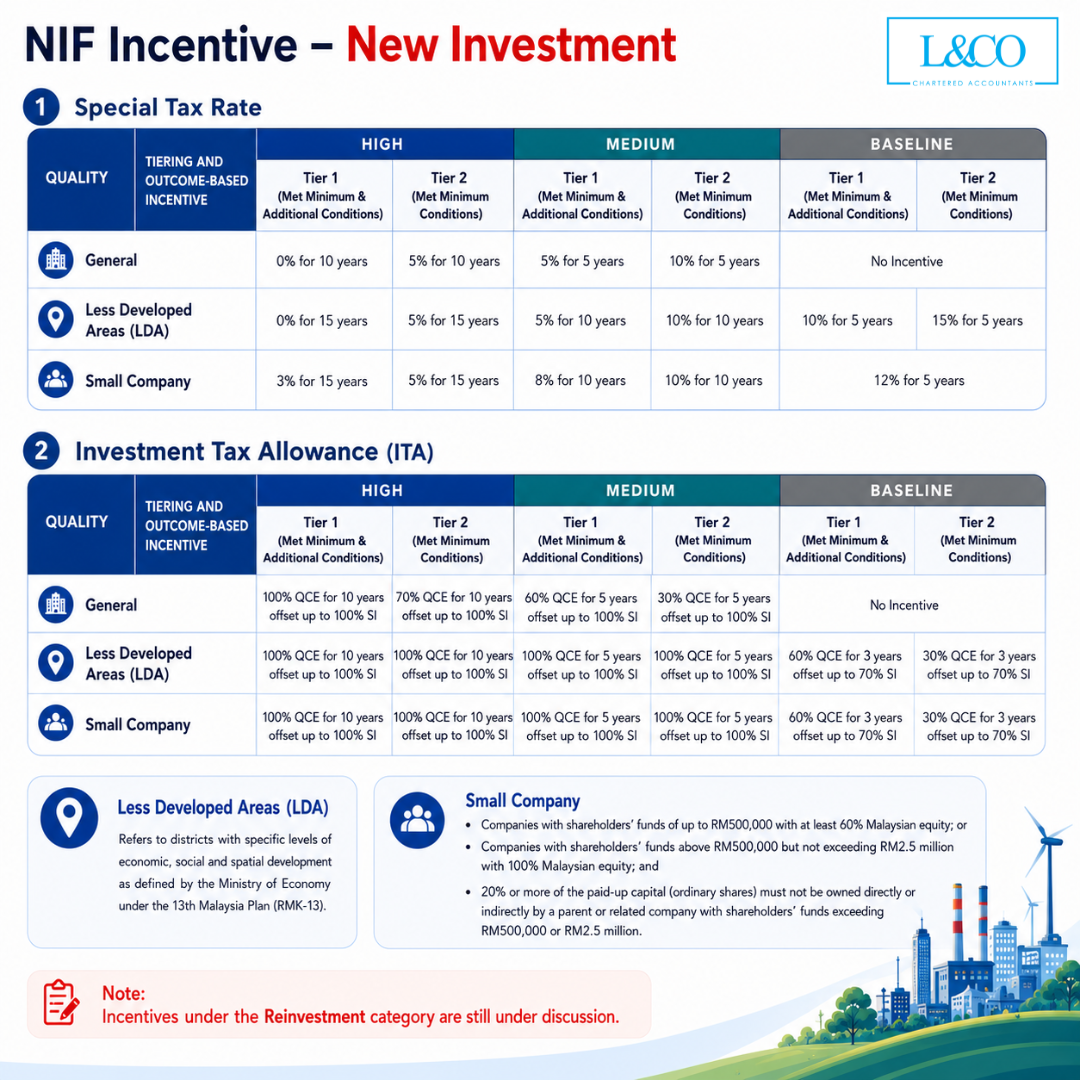

NIF Tax Incentives (Special Tax Rate & Investment Tax Allowance)

The NIF offers two main tax incentive schemes:

A. Special Tax Rate (STR)

Eligible companies may enjoy preferential corporate tax rates for different incentive periods based on their quality level and investment outcomes.

Companies are assessed under three quality categories:

- High

- Medium

- Baseline

Each category is further divided into Tier 1 and Tier 2, depending on whether the company meets the required conditions and additional performance criteria.

Different incentive packages are available for:

- General Companies

- Less Developed Area (LDA) Companies

- Small Companies

B. Investment Tax Allowance (ITA)

Companies that incur Qualified Capital Expenditure (QCE) may qualify for an Investment Tax Allowance (ITA).

Depending on the company’s quality level and investment performance, the allowance may offset:

- Up to 100% of Statutory Income (SI), or

- Up to 70% of Statutory Income (SI)

The actual incentive granted depends on the company’s assessed quality level and investment outcomes.

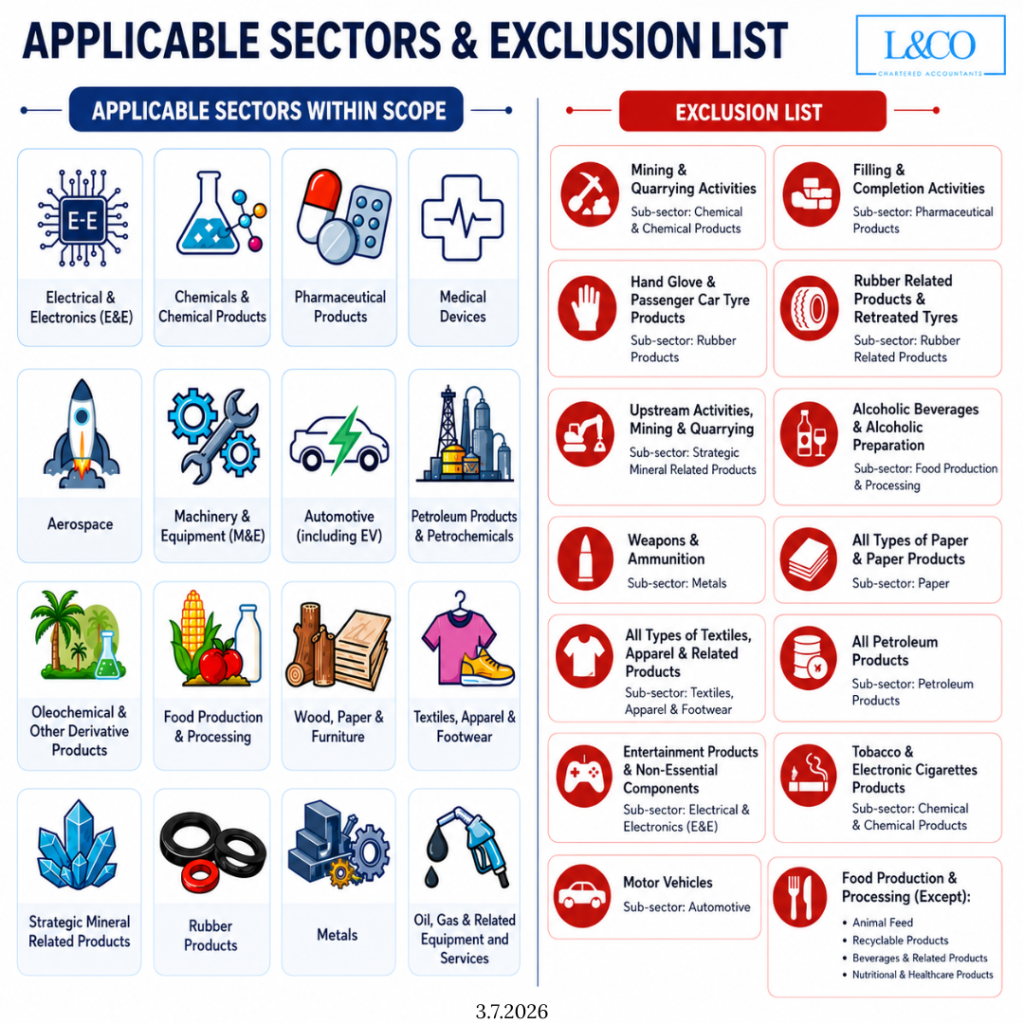

Which Industries Are Eligible?

The NIF focuses on promoting investments in high-value industries, including:

- Electrical & Electronics (E&E)

- Chemicals & Chemical Products

- Pharmaceuticals

- Medical Devices

- Aerospace

- Machinery & Equipment (M&E)

- Automotive (including Electric Vehicles)

- Petroleum & Petrochemicals

- Oleochemicals

- Food Manufacturing

- Timber, Paper & Furniture

- Textile, Apparel & Footwear

- Critical Minerals

- Rubber Products

- Metal Products

- Oil & Gas Equipment & Services

Which Industries Are Excluded?

The following industries are generally not eligible under the NIF:

- Mining & Quarrying

- Rubber Gloves

- Passenger Vehicle Tyres

- Upstream Oil & Gas

- Alcoholic Beverages

- Ammunition & Weapons

- Paper Products

- Textile Products

- Petroleum Products

- Tobacco & Vape Products

- Gaming Components

- Passenger Vehicles

- Selected Food Processing Activities

Businesses should verify whether their industry falls within the eligible scope before applying.

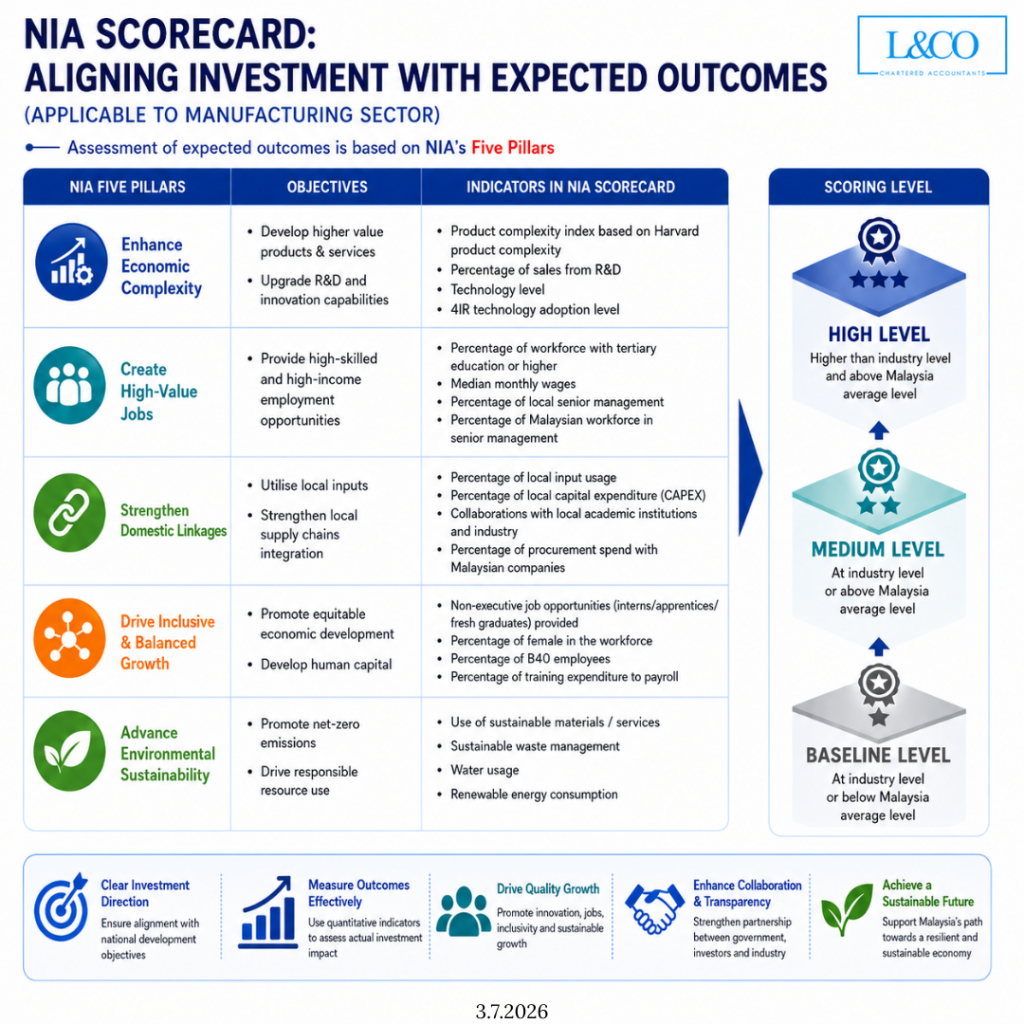

4. How Does the NIA Scorecard Affect Incentives?

The NIA Scorecard serves as the core assessment tool under the NIF, evaluating investment projects based on five strategic pillars:

- Economic Complexity

Promoting higher value-added products, advanced manufacturing, and technological innovation. - High-Value Employment

Creating skilled, high-income employment opportunities for Malaysians. - Domestic Linkages

Strengthening local sourcing, supplier development, and domestic supply chains. - Inclusive Development

Supporting balanced regional growth and broader socio-economic development. - Sustainable Practices

Encouraging ESG initiatives, green manufacturing, and long-term sustainability.

Based on the assessment, companies will be classified into one of three levels:

- High

- Medium

- Baseline

The final classification determines the level of tax incentives available.

5. How to Apply for a Manufacturing Licence (ML) and ICA10?

Applications should be submitted through MIDA.

Manufacturing Licence (ML)

A Manufacturing Licence may be required if the company meets either of the following criteria:

- Shareholders’ Funds of RM2.5 million or above, or

- Employs 75 or more full-time paid employees

ICA10 (Manufacturing Licence Exemption)

Companies may apply for ICA10 if they satisfy both of the following conditions:

- Shareholders’ Funds do not exceed RM2.5 million, and

- Employ fewer than 75 full-time paid employees

All applications must be submitted via MIDA’s official application system.