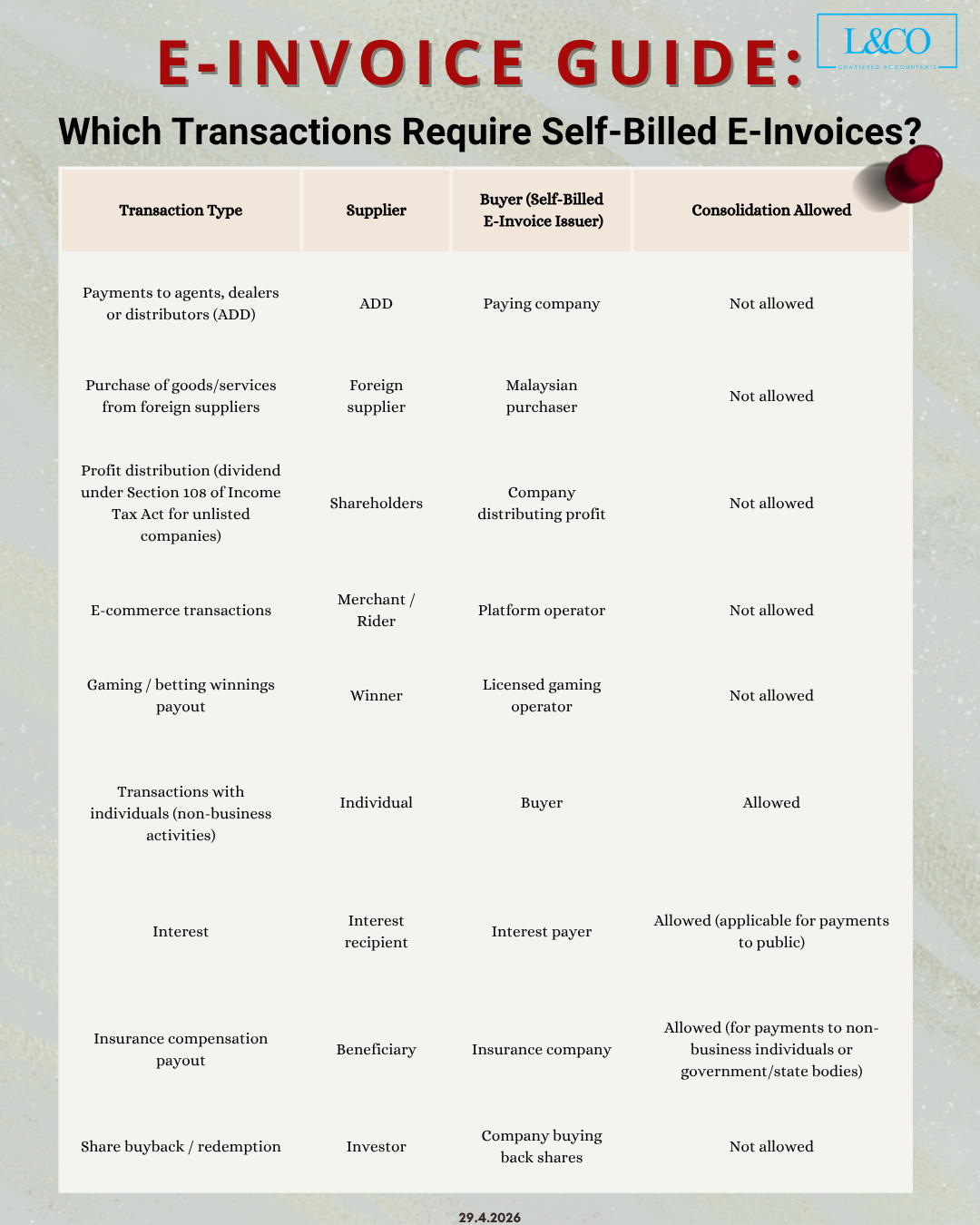

Under Malaysia’s E-Invoice framework, certain prescribed transaction types require the buyer to issue an e-Invoice on behalf of the supplier (Self-Billed E-Invoice). The following outlines the main applicable scenarios:

1. Mandatory Issuance (Consolidation Not Allowed)

The following transactions must be self-billed on a per-transaction basis and cannot be consolidated:

- Payments to agents, dealers, or distributors (ADD)

- Purchases of goods or services from foreign suppliers

- Distribution of dividends by non-listed companies (pursuant to Section 108 of the Income Tax Act)

- E-commerce transactions (issued by platform operators under applicable models)

- Payouts from gaming or betting activities

- Share buybacks or redemption of shares

2. Permitted Issuance (Consolidation Allowed Under Conditions)

The following transactions may be self-billed, and consolidation is allowed subject to conditions:

- Transactions with individuals not carrying on a business

- Interest payments to the general public

- Insurance claim payouts to individuals or government entities

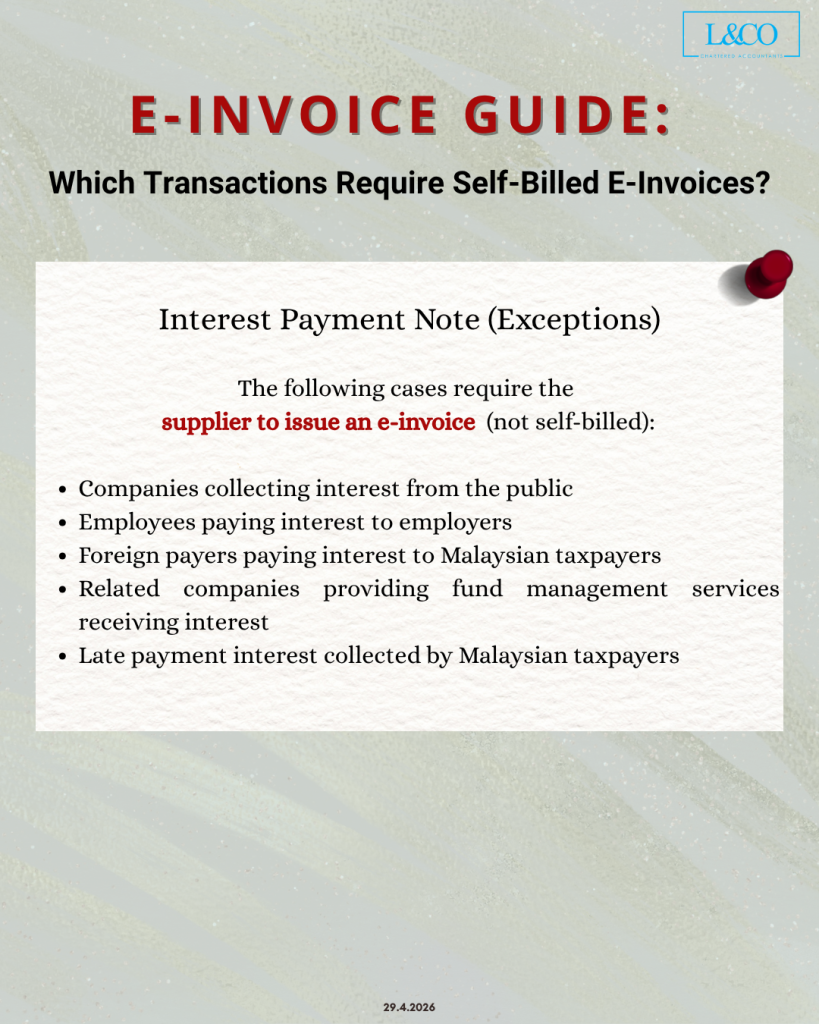

3. Exceptions for Interest Payments

For interest-related transactions, the following do not qualify for Self-Billed E-Invoice, and the supplier must issue the e-Invoice:

- Businesses providing loans to the public and earning interest

- Interest paid by employees to employers

- Interest paid by foreign payers to Malaysian taxpayers

- Interest paid to related companies providing treasury services

- Late payment interest imposed by Malaysian taxpayers

4. Summary

The core principle of Self-Billed E-Invoice is that it applies to prescribed scenarios where the buyer is required to issue the e-Invoice on behalf of the supplier.

However, not all similar transactions qualify. Businesses should assess the nature of each transaction carefully to ensure full compliance with E-Invoice requirements.

**Data updated on 30.4.2026