Many individuals operating small businesses or working as freelancers in Malaysia commonly assume that if they have not registered with SSM, they have no obligations towards LHDN.

However, this misconception is not only inaccurate but may also expose individuals to legal and financial consequences arising from non-compliance with tax regulations. This article aims to clarify the relationship between SSM registration and tax reporting obligations, helping self-employed individuals better understand their responsibilities under Malaysian tax laws.

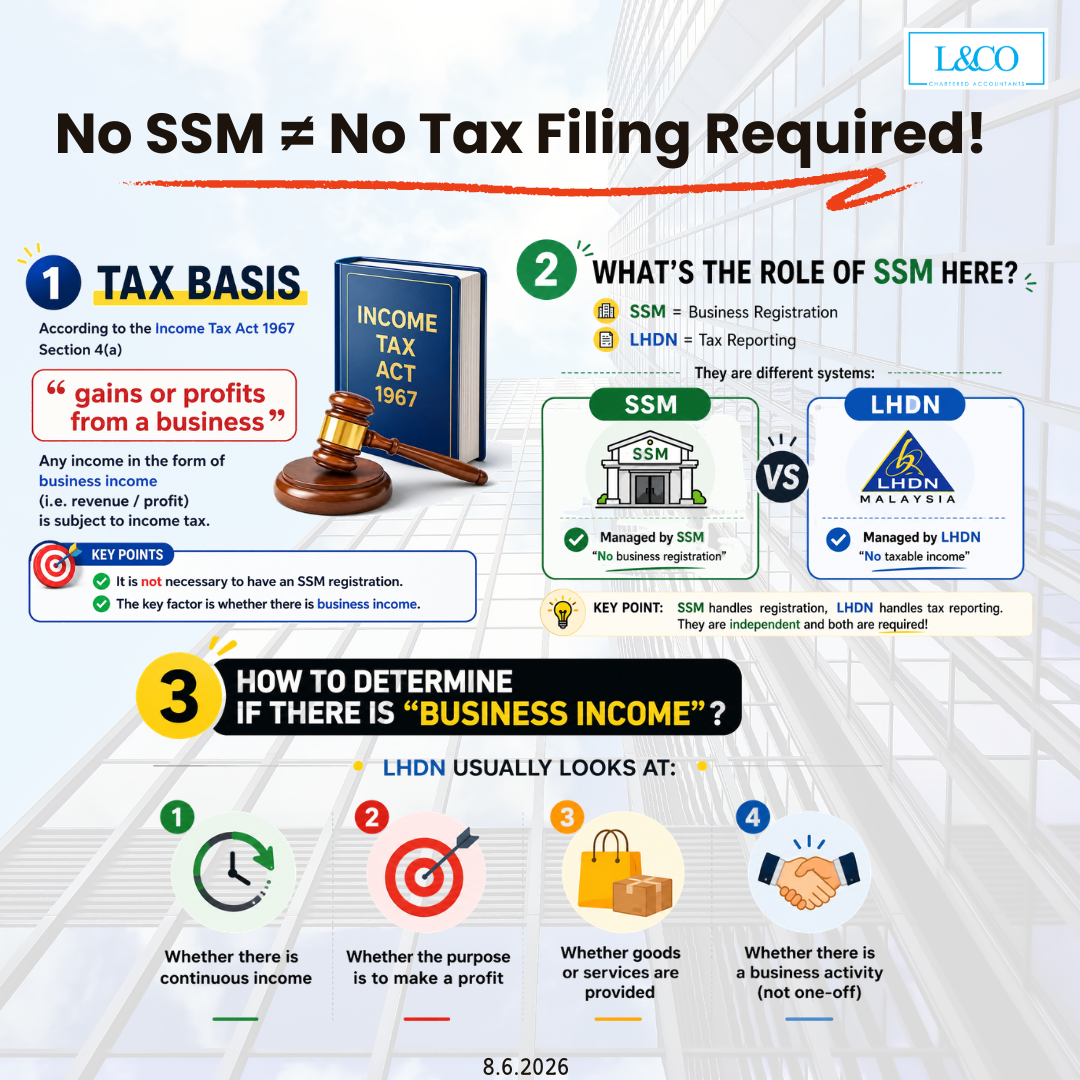

1. The Legal Basis for Taxation

Under Section 4(a) of the Income Tax Act 1967, income tax is imposed on gains or profits derived from a business.

Importantly, there is no provision within the Income Tax Act 1967 that states a person must possess an SSM registration before becoming liable for tax, nor does the absence of an SSM registration exempt a person from taxation.

In other words, tax liability is determined by the nature of the income earned, not by the registration status of the business.

If your income is considered business income, you may be legally required to report and declare such income to LHDN regardless of whether you have registered your business with SSM.

2. SSM and LHDN: Two Separate Regulatory Systems

The misunderstanding often arises from confusing the roles of SSM and LHDN. Although both are government agencies, their functions are entirely different.

- SSM:Regulates whether a business is properly registered under Malaysian law

- LHDN:Regulates whether a person has taxable income and complies with tax reporting obligations

Simply put:

- SSM regulates whether you have registered a business.

- LHDN regulates whether you have taxable income.

There is no direct correlation between the two.

You may not have an SSM registration but still be required to report income to LHDN. Conversely, even if you have an SSM registration, you may not be liable for tax if no taxable income is generated.

3. How Does LHDN Determine Whether You Are Carrying on a Business?

In the absence of a formal business registration, LHDN generally evaluates the nature of an activity based on several key factors to determine whether it constitutes a business.

1. Regularity of Income

Is the income earned on a recurring and continuous basis?

Income that is generated consistently and systematically is more likely to be regarded as business income than income arising from isolated or one-off transactions.

2. Profit Motive

Is the activity conducted with the intention of making a profit?

Where there is a clear commercial objective to generate earnings, the activity is more likely to be classified as a business.

3. Provision of Goods or Services

Are goods or services being provided to customers or clients?

The provision of products or services is one of the fundamental characteristics of a business activity.

4. Commercial Nature of the Activity

Does the activity involve an organized and repeatable business model rather than a single casual transaction?

A systematic approach to generating income generally indicates the existence of a business.

If these factors are present, LHDN may regard the income as business income and require it to be declared accordingly.

4. Common Self-Employment Situations and Tax Treatment

The following examples illustrate situations where income may be treated as business income even without an SSM registration.

1. Freelance Designers

Individuals who regularly undertake design, poster creation, branding, or creative projects for clients and maintain a structured pricing model may be regarded as carrying on a business due to the recurring and profit-oriented nature of their activities.

2. Online Sellers (Shopee, TikTok Shop, etc.)

Online sellers who consistently process orders, communicate with customers, manage inventory, arrange deliveries, run advertisements, or conduct livestream sales are generally operating a business regardless of whether they are registered with SSM.

3. Delivery Riders and Platform Workers

Individuals who regularly accept jobs through delivery or gig economy platforms and earn service fees from each completed task are engaged in income-generating activities that may constitute a business.

4. Property Agents

Property agents who continuously source clients, conduct marketing activities, and earn commission income upon successful transactions are typically considered to be carrying on a business.

5. Content Creators

Individuals earning income through brand sponsorships, affiliate marketing, advertising collaborations, or paid promotional activities are often engaged in commercial activities that may be classified as business income.

Key Principle

Income + Customers + Continuity = Potential Business Activity

Where these elements exist, the income is likely to be regarded as business income for tax purposes.

5. Which Tax Return Should You File: Form B or Form BE?

Self-employed individuals must ensure that they submit the correct tax return based on the nature of their income.

Form BE

- Salaried Employees

- Employment Income Only

Form B

- Self-Employed Individuals / Business Owners

- Includes Business Income

If your annual income includes any form of business income, you should generally submit Form B instead of Form BE.

Submitting the wrong tax return may result in compliance issues, additional assessments, penalties, or requests for amendment by LHDN.